Know Your Rights: Protecting Yourself from Debt Collection Harassment

Dealing with debt can be overwhelming, especially when you're contacted by aggressive or persistent debt collectors. Many consumers are unaware of the protections available to them under federal law, particularly the Fair Debt Collection Practices Act (FDCPA). Understanding your rights can be the first step toward stopping abuse and regaining control over your financial situation.

One frequent complaint among consumers today is Omni Point Capital Debt Collection Harassment. Whether it’s repeated calls, threats, or false representations, such tactics may be illegal under the FDCPA. Knowing what constitutes harassment and how to respond can empower you to take back control.

What is the FDCPA?

The Fair Debt Collection Practices Act is a federal law enacted in 1977 to curb abusive behavior by third-party debt collectors. It outlines what collectors can and cannot do when attempting to recover debts and provides specific legal remedies for consumers subjected to unfair practices.

The FDCPA applies only to personal, family, and household debts. This includes credit card debts, mortgages, medical bills, and other household-related financial obligations. Importantly, it does not cover business debts.

Common Violations Under the FDCPA

If you’re being harassed by a debt collector, you should understand the types of behaviors that may violate your rights. Here are some of the most common FDCPA infractions:

-

Repeated or Excessive Contact: Calling multiple times a day or at odd hours (before 8 AM or after 9 PM) is generally considered harassment.

-

Use of Threatening Language: Debt collectors may not threaten violence, arrest, or legal action that they do not intend to take or cannot legally take.

-

False or Misleading Representations: It is illegal for collectors to misrepresent who they are, the amount you owe, or any legal consequences.

-

Contacting Third Parties: Collectors are not allowed to discuss your debt with anyone other than your spouse or attorney, except to obtain contact information.

-

Ignoring a Written Request to Cease Communication: If you ask them in writing to stop contacting you, they must comply except for a few legal notifications.

Steps to Take if You're Being Harassed

If you believe a collector has violated your rights, here’s what you can do:

1. Document Everything

Start by keeping a detailed record of all communications. Note the date, time, caller’s name, what was said, and any threatening or misleading statements. Save voicemails, emails, and letters.

2. Request Written Verification

Under the FDCPA, you have the right to request written validation of the debt. This forces the collector to prove that the debt is legitimate and that you owe it. You must make this request within 30 days of their initial contact.

3. Send a Cease and Desist Letter

You can send a written request asking the collector to stop contacting you. Once they receive this letter, they may only reach out to inform you of specific actions like a lawsuit.

4. Report the Abuse

If the harassment continues, you can file complaints with:

-

The Consumer Financial Protection Bureau (CFPB)

-

The Federal Trade Commission (FTC)

-

Your state’s attorney general

These agencies can investigate and potentially sanction the collector.

5. Consult an Attorney

If the harassment continues or has caused emotional or financial damage, consulting a consumer protection attorney can be a smart move. They can help you file a lawsuit and may even help you recover damages.

Legal Remedies Available to You

If your rights under the FDCPA are violated, you may be entitled to:

-

Actual damages: Compensation for out-of-pocket costs and emotional distress.

-

Statutory damages: Up to $1,000 even without proof of actual damages.

-

Attorney’s fees and court costs: If you win the case, the collector may have to cover your legal expenses.

How to Avoid Future Issues with Debt Collectors

The best long-term defense against abusive debt collection is sound financial management. Here are a few tips:

-

Stay informed: Review your credit report regularly to ensure all information is accurate.

-

Communicate proactively: If you're struggling to pay a debt, reach out to the original creditor or debt collector early. Many will work with you on a payment plan.

-

Know your rights: Familiarize yourself with the FDCPA and state-specific laws that provide additional protections.

-

Avoid shady debt settlement companies: Some organizations promise to "settle your debt" but may charge high fees or worsen your credit situation.

Final Thoughts

Debt collection is a legal process, but that doesn’t mean consumers should tolerate harassment or abuse. The FDCPA exists to protect you from exactly that. If you find yourself on the receiving end of persistent, aggressive, or dishonest collection tactics, you have the right—and the tools—to fight back.

Remember, help is available. Understanding your rights, documenting everything, and seeking legal counsel when necessary are powerful steps toward protecting yourself and holding bad actors accountable.

Κατηγορίες

Διαβάζω περισσότερα

"In-Depth Study on Executive Summary Enhanced Water Market Size and Share The global enhanced water market size was valued at USD 9.03 billion in 2024 and is expected to reach USD 19.51 billion by 2032, at a CAGR of 10.1% during the forecast period Enhanced Water Market research report acts as a very significant constituent of business...

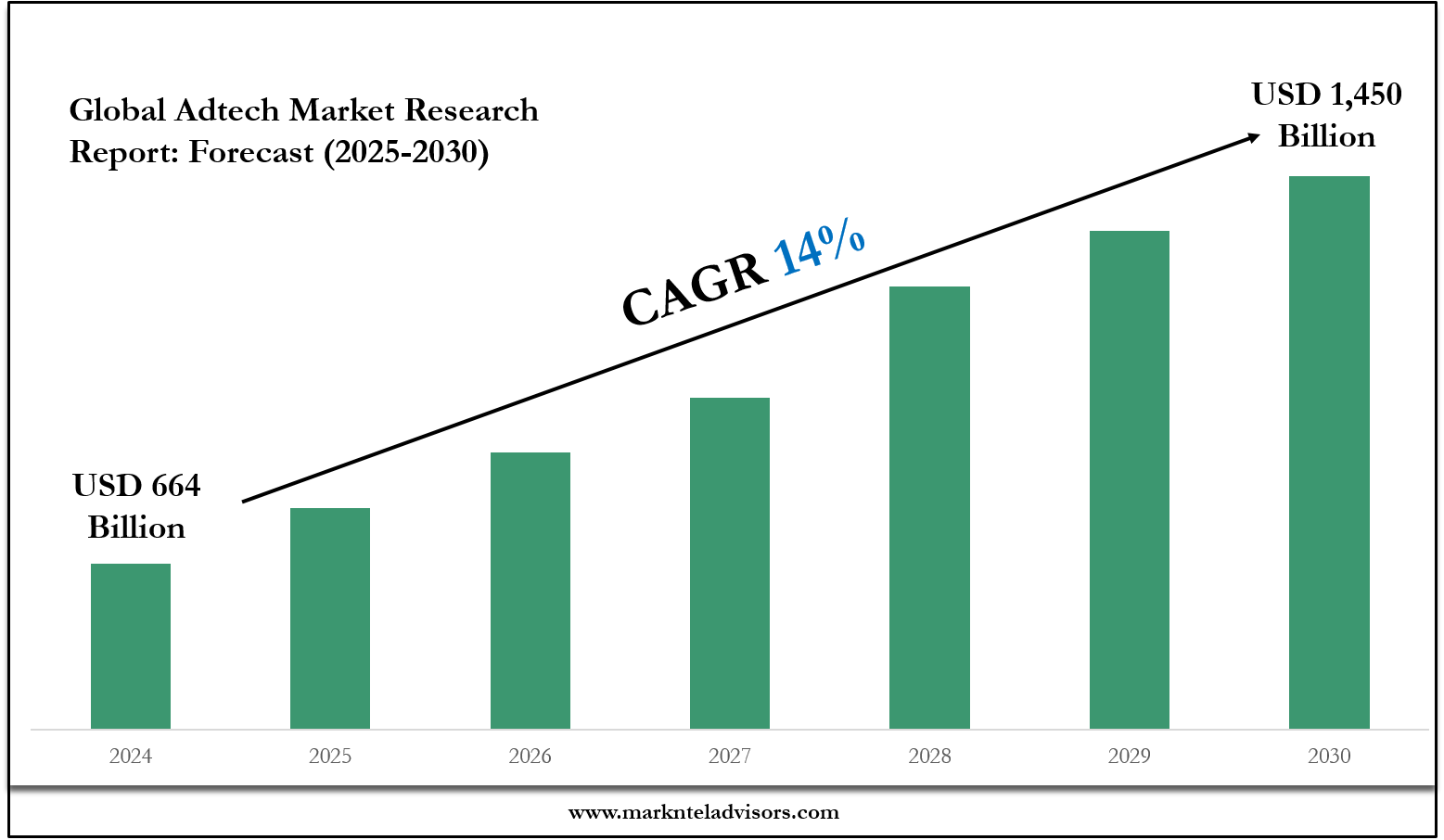

Overview of the Global Adtech Market: Gain data-driven insights into the Global Adtech Market Size, trends, and forecasts. This in-depth report delivers expert analysis of market drivers, segmentation, and emerging opportunities. It highlights key metrics and actionable findings in a professional, easy-to-scan format. Key statistics (market size, growth rates, share by segment) are presented...

Primo TRT Gummies Male Enhancement are made from a blend of natural ingredients that are carefully selected for their ability to promote male sexual health. These ingredients may include herbs, vitamins, minerals, and other nutrients known for their aphrodisiac and performance-enhancing properties. Unlike traditional pills or capsules, these gummies offer a convenient and...

I thought wedding entertainment booking would be easy. Like, “Oh, I’ll just Google a DJ, maybe throw in a live band if the budget allows, and we’re good.” That was the fantasy. Reality? Not even close. Booking entertainment for your wedding isn’t just about filling a time slot with music. It’s a whole emotional rollercoaster of expectations, weird vendor...

When customers walk into a store or browse products online, the first thing that grabs their attention isn’t always the product itself—it’s the packaging. Captivating visual & packaging design has become one of the most powerful tools for brands to stand out in crowded markets, connect emotionally with buyers, and inspire loyalty. In today’s competitive world,...