Global Liquefied Natural Gas Market Outlook

The liquefied natural gas (LNG) market is experiencing accelerated growth worldwide, driven by the increasing shift toward low-carbon energy sources, rising global energy demand, and the need for energy security. As nations seek to diversify their energy mix and reduce dependence on coal and oil, LNG has emerged as a key transitional fuel offering cleaner combustion, efficient transport, and scalability. According to Market Research Future, the LNG market is poised for significant expansion through 2032, supported by infrastructure development, technology innovation, and expanding end-use applications.

Market Dynamics

The global LNG market is witnessing dynamic transformation, catalyzed by several converging trends. First, the rising global commitment to decarbonization is pushing countries to adopt fuels that emit less carbon dioxide and pollutants. LNG, which produces up to 40% fewer carbon emissions than coal, has gained widespread acceptance as a cleaner-burning alternative for power generation, transportation, and industrial use.

Second, surging demand from Asia-Pacific nations, particularly China, India, South Korea, and Japan, is fueling LNG import growth. These economies are ramping up LNG imports to meet rising electricity consumption and industrial demand while phasing out coal-fired plants. China, the world's top LNG importer, is expanding its regasification capacity and signing long-term supply contracts to meet its ambitious climate goals.

Third, geopolitical disruptions—such as the Russia-Ukraine conflict—have highlighted the vulnerabilities of traditional pipeline gas supplies, especially in Europe. This has led to a renewed push for LNG terminals and storage infrastructure, allowing countries to diversify their sources and enhance energy resilience. European nations like Germany, Poland, and the Netherlands are investing in floating storage regasification units (FSRUs) and long-term LNG procurement deals.

Moreover, technological advancements are shaping market growth. Innovations in liquefaction and regasification processes, cryogenic transport, and modular terminals have made LNG projects more cost-effective and scalable. Small-scale LNG is becoming viable for remote locations, marine bunkering, and off-grid industrial applications, opening new markets and revenue streams.

Competitive Landscape

The LNG market is highly competitive and characterized by a mix of established energy giants, state-owned enterprises, and emerging players leveraging innovation and strategic partnerships. Key participants include Shell plc, Chevron Corporation, ExxonMobil Corporation, TotalEnergies SE, BP plc, QatarEnergy, and Cheniere Energy, Inc.

QatarEnergy remains the world’s leading LNG exporter, with its North Field expansion project set to boost its capacity significantly over the next decade. Shell and TotalEnergies are actively investing in integrated LNG value chains that span exploration, liquefaction, shipping, and regasification. Cheniere Energy has positioned itself as a dominant force in the U.S. LNG export space, with multiple trains operating along the Gulf Coast.

Strategic joint ventures and long-term supply agreements are central to the competitive strategies of these companies. For example, ExxonMobil and QatarEnergy are collaborating on mega liquefaction projects, while Asian utilities and trading companies are locking in 15–20 year LNG supply contracts to hedge against price volatility.

In addition, midstream players are expanding their portfolios to include LNG shipping and storage services. Investment in LNG-fueled ships, floating LNG units (FLNGs), and mobile regasification systems is increasing, driven by global marine regulations that cap sulfur emissions and promote cleaner fuels.

Environmental performance is also becoming a key differentiator. Companies are adopting carbon-neutral LNG, offsetting emissions through renewable projects and carbon capture and storage (CCS) initiatives. Transparency in lifecycle emissions and sustainability certification is emerging as a critical factor in securing long-term customers, particularly in Europe and Japan.

Regional Insights

Asia-Pacific dominates the LNG market, accounting for the bulk of global demand. Countries like China, India, South Korea, and Japan are scaling up LNG imports to reduce coal reliance and support industrial expansion. These nations are building new terminals, expanding storage, and upgrading pipeline connectivity to accommodate growing LNG inflows.

North America, particularly the U.S., has transformed into a major LNG exporter, leveraging its vast shale gas reserves and favorable infrastructure. The U.S. now supplies LNG to both European and Asian markets, enhancing its geopolitical influence in global energy trade. Ongoing investments in liquefaction capacity and LNG bunkering facilities continue to strengthen the region’s market position.

Europe has become a key growth market amid the reorientation of gas sourcing strategies away from Russia. Countries are fast-tracking terminal construction and FSRU deployment to ensure energy supply security. The EU’s REPowerEU plan and decarbonization goals are also increasing LNG’s role as a bridge fuel in the energy transition.

The Middle East, particularly Qatar, Oman, and the UAE, remains a critical supply hub, while Africa is emerging as a promising region with new LNG projects in Mozambique, Nigeria, and Senegal gaining investor interest. Latin America is also entering the LNG space with demand growth in Brazil, Chile, and Argentina, driven by energy diversification efforts.

Future Outlook

The global liquefied natural gas market is expected to evolve rapidly over the next decade, playing a pivotal role in the transition to a low-carbon energy system. As demand for cleaner, reliable, and flexible energy grows, LNG will remain central to global energy strategies, especially in emerging economies and regions undergoing power sector transformation.

New LNG use cases—including heavy-duty transport, industrial heating, and hydrogen production—are expanding the market’s scope. Moreover, digitalization and AI-driven monitoring tools are optimizing operations across the LNG value chain, improving safety, efficiency, and emissions tracking.

Sustainability, supply security, and innovation will be the defining pillars of competitive advantage. Companies that can balance affordability with environmental performance and adaptability will lead the market.

To explore detailed forecasts, market segmentation, and strategic insights, visit Market Research Future.

More Trending Reports:

الأقسام

إقرأ المزيد

Whitefield, a modern area in India, offers luxurious Whitefield call girl services for those seeking sensual enjoyment. It is a hub for influential politicians and successful businesspeople, which reflects the high standards of the call girls available. These call girls are trained to meet both physical and emotional needs and come in various types, including mature housewives and...

The upcoming sequel Helldivers 2 is already generating buzz among fans for its expanded arsenal, refined mechanics, and challenging enemy encounters. Among these new challenges, the Introducing the Illuminate: Helldivers 2's New Enemy Faction stands out as a game-changing addition. In this article, we’ll break down what makes the Illuminate a unique and formidable threat on the...

Vitacore CBD Gummies Review, Benefits and Where to Buy ORDER NOW : https://healthyifyshop.com/OrderVitacoreCBDGummies Vitacore CBD Gummies offer a natural, effective, and enjoyable way to incorporate the benefits of CBD into your wellness routine. Whether you're seeking relief from stress, improved sleep, or general health support, these gummies provide a convenient...

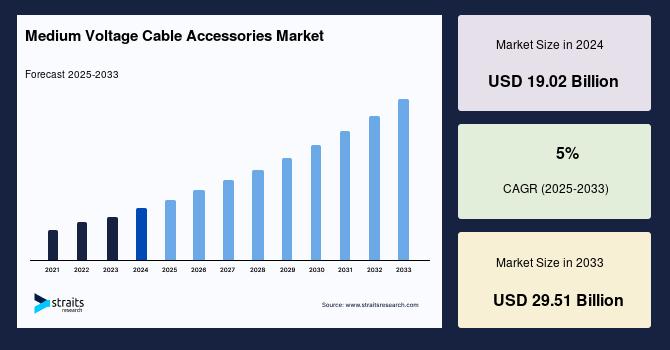

Worldwide Medium Voltage Cable Accessories Market Scope [110 Pages Report] Comprising over 150 pages of meticulous examination, the report offers an in-depth analysis. Additionally, this comprehensive market report encompasses projected market dimensions and trends pertaining to various countries within key global regions. According to StraitsResearch, the global medium voltage cable...

In the ever-expanding world of online betting, security, user-friendliness, and accessibility are at the forefront of what makes a platform truly exceptional. Lotus365 has steadily positioned itself as a pioneer in delivering a digital betting experience that is not only secure but also tailored to meet the diverse needs of its users. From seamless login access to unmatched betting odds,...