What to Know Before Applying for a Wedding Loan

Your wedding is one of the most important days of your life—but it can also be one of the most expensive. From the venue and catering to the dress and décor, costs can add up quickly. If you’re looking for a way to finance your big day without draining your savings, a wedding loan might be an option worth considering.

But before you sign on the dotted line, it’s important to understand what you’re getting into. A wedding loan is a financial commitment, and making an informed decision can save you a lot of stress (and money) down the road. Here’s what you should know before applying for wedding loan.

1. What Is a Wedding Loan?

A wedding loan is essentially a personal loan that’s used to cover wedding-related expenses. It’s an unsecured loan, which means you don’t have to offer collateral like a car or home. You receive a lump sum upfront and repay it in fixed monthly installments over a set term, typically between 1 to 5 years.

While some lenders market personal loans specifically as “wedding loans,” there’s no special category—these loans work the same way as any other personal loan.

2. Check Your Credit Score First

Your credit score plays a big role in determining whether you’ll be approved for a loan and what interest rate you’ll receive. A higher score usually means lower interest rates and better loan terms.

Before applying, check your credit report and make sure there are no errors. If your score is low, consider taking a few months to improve it by paying down debt and making all payments on time. This can make a significant difference in the long run.

3. Compare Loan Offers

Don’t go with the first offer you receive. Take time to shop around and compare options from banks, credit unions, and online lenders. Look closely at the following:

-

Interest rates (APR)

-

Repayment terms

-

Fees (origination, prepayment, or late payment)

-

Loan amount limits

Many lenders allow you to prequalify with a soft credit check, which won’t impact your credit score. Use this feature to compare offers without committing.

4. Know Your Budget and Borrow Responsibly

Before applying for a loan, create a detailed wedding budget. Figure out how much you need to borrow—and no more. Remember, the more you borrow, the more interest you’ll pay over time.

Try to strike a balance between the wedding of your dreams and financial stability. Ask yourself:

-

Can I afford the monthly payments?

-

What will this loan cost me in total?

-

Am I sacrificing future goals like a home, travel, or savings?

Borrowing responsibly means making sure the loan won’t become a burden after the honeymoon is over.

5. Understand the Total Cost of the Loan

It’s not just about the amount you borrow—it’s about how much you’ll repay overall. For example, a $15,000 loan at a 12% APR over 5 years could cost you over $4,000 in interest alone.

Use online loan calculators to estimate the total cost, and read the fine print to ensure you understand the full repayment schedule and any potential penalties.

6. Consider Alternatives

Before committing to a wedding loan, consider other financing options:

-

Saving up over time and delaying the wedding slightly

-

Using a zero-interest credit card (if you’re confident you can repay quickly)

-

Cutting costs by trimming your guest list or opting for off-season dates

-

Asking family for help (if appropriate and comfortable)

While a loan can provide quick relief, it shouldn’t be your only plan.

Final Thoughts

A wedding loan can be a helpful tool to bring your celebration to life—but it’s not a decision to take lightly. By understanding how wedding loans work, evaluating your finances honestly, and exploring your options, you can avoid unnecessary debt and start your married life on a strong financial footing.

Категории

Больше

Als vastgemaakte liefhebber van online weddenschappen, ben je waarschijnlijk op zoek naar de beste crypto bookmakers 2025. In dit artikel gaan we dieper in op de ontwikkelingen in de wereld van crypto-weddenschappen en wat je kunt verwachten in de toekomst. We zullen de krachten vergelijken tussen verschillende crypto bookmakers, waaronder CoinCasino, Instant Casino, Mega Dice en Lucky Block,...

"Global Executive Summary Europe Effervescent Tablet Market: Size, Share, and Forecast Europe effervescent tablet market is expected to gain market growth in the forecast period of 2021 to 2028. Data Bridge Market Research analyses that the market is growing with a CAGR of 7.6% in the forecast period of 2021 to 2028 and is expected to reach USD 4,229.89 million by 2028. The advantages of...

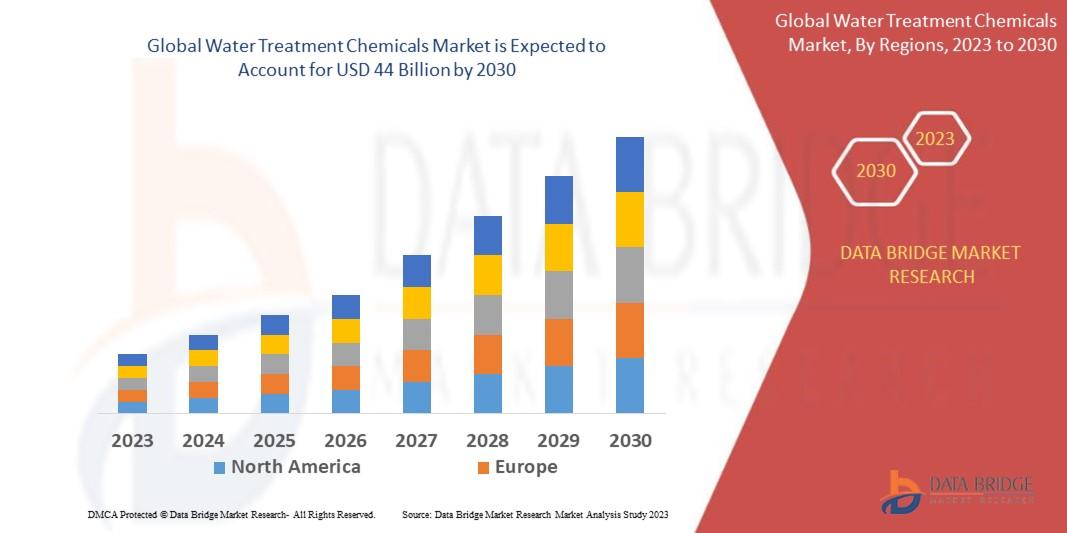

The Water Treatment Chemicals Market has become a cornerstone of global environmental sustainability, industrial operations, and public health management. With rising concerns about water scarcity, pollution, and the increasing demand for clean water across residential, commercial, and industrial applications, the use of advanced chemical solutions for water purification and...

The Food Allergens and Intolerance Testing Market Study delivers a comprehensive assessment of the worldwide market, covering its structure, key trends, and future potential. This report provides a detailed examination of the market's current valuation, growth drivers, and the competitive strategies of leading players. It is designed to equip stakeholders with the knowledge necessary...

Infertility, while common, is deeply personal. Couples facing challenges with conceiving often search tirelessly for the right fertility clinic — one that combines expertise, technology, empathy, affordability, and high success rates. In East Delhi, one name that often comes up is Dr Bhavana Mittal and her clinic, Shivam IVF & Infertility Centre (Shivam Surgical & Maternity...