Policy Limit Verification: Key Questions to Ask an Insurance Company

Insurance is a critical safety net for both individuals and businesses, providing financial protection against unexpected losses. However, having an insurance policy is only part of the equation; understanding the coverage limits and how they apply is equally crucial.

Policy limit verification ensures that your insurance coverage aligns with your needs and expectations. This process involves reviewing your insurance policies, confirming coverage limits, and asking the right questions to the insurance company. Failure to properly verify policy limits can lead to underinsurance, coverage gaps, or unexpected out-of-pocket expenses in the event of a claim.

Understanding Policy Limits

Before diving into the questions to ask, it is essential to understand what policy limits are. In insurance, a policy limit is the maximum amount an insurer will pay for a covered loss. Policy limits can vary depending on the type of insurance, such as auto, homeowners, health, or commercial liability insurance. There are typically three types of limits:

Per Occurrence Limit: The maximum amount the insurance company will pay for a single incident or claim.

Aggregate Limit: The total amount an insurer will pay over the policy period, usually one year, for multiple claims.

Sublimits: Specific limits that apply to particular types of coverage or losses within the policy. For example, a homeowner’s policy may have a sublimit for jewelry or electronics.

Verifying these limits is crucial because exceeding them could leave you personally liable for costs not covered by insurance.

Why Policy Limit Verification Matters

Policy limit verification ensures that your coverage adequately addresses your risks. It helps in:

Avoiding Underinsurance: Insufficient coverage may leave you responsible for losses exceeding the policy limits.

Preventing Coverage Gaps: Misunderstandings about what is covered can result in unexpected claim denials.

Ensuring Compliance: Certain business and contractual agreements require proof of insurance with specific limits.

Peace of Mind: Knowing your coverage limits allows you to plan and manage risks effectively.

Key Questions to Ask Your Insurance Company

When verifying policy limits, it is essential to ask detailed questions. Here are the key inquiries to consider:

1. What Are the Policy Limits for Each Type of Coverage?

Start by asking for a breakdown of coverage limits for each type of coverage in your policy. For instance, in an auto insurance policy, verify liability limits, collision, comprehensive, and uninsured/underinsured motorist coverage. For businesses, ensure commercial general liability, professional liability, and property coverage limits are clearly stated.

2. Are These Limits Per Occurrence or Aggregate?

Clarify whether the stated limits apply per incident or as a cumulative total over the policy term. For example, a liability limit might be $1 million per occurrence but $2 million in aggregate annually. Understanding this distinction is critical, particularly for businesses or individuals with frequent risk exposure.

3. Are There Any Sublimits or Special Conditions?

Ask about sublimits that may apply to specific items or scenarios. Many policies have restrictions on certain types of property, like electronics, fine art, or cash. Knowing these limits helps you determine whether additional coverage, such as endorsements or riders, is necessary.

4. Does the Policy Cover Multiple Claims?

It is important to understand how multiple claims affect your coverage. Some policies reduce coverage amounts with each claim filed, while others maintain full limits for each occurrence. Clarifying this will help avoid surprises when multiple incidents happen within a policy period.

5. Are There Exclusions or Limitations?

Insurance policies often have exclusions—situations or types of losses not covered. Ask the insurer to explain all relevant exclusions and how they might affect your policy limits. For example, natural disasters or certain high-risk activities might not be covered unless you have additional riders.

6. How Do Deductibles Affect My Coverage?

Deductibles are the amount you must pay out-of-pocket before insurance coverage kicks in. While not technically part of policy limits, understanding deductibles is crucial because they directly impact your financial responsibility in the event of a claim.

7. Are My Policy Limits Adequate for Current Risks?

Situations change over time, whether due to increased assets, business expansion, or inflation. Ask your insurance company if your current policy limits reflect your present needs. Adjusting your coverage proactively ensures you are not underinsured when a loss occurs.

8. How Are Claims Paid Out Relative to Limits?

Verify the method of claims payment. Some policies pay actual cash value (ACV), which considers depreciation, while others pay replacement cost. Understanding this distinction helps you gauge whether your policy limits will realistically cover replacement or repair costs.

9. Are There State or Legal Requirements for Coverage?

Some states mandate minimum coverage amounts for certain types of insurance, such as auto liability or workers’ compensation. Confirm with your insurance company that your policy meets or exceeds legal requirements to avoid penalties or legal issues.

10. Can Policy Limits Be Increased or Adjusted?

If your needs change, ask about options to increase limits. This could involve adjusting liability limits, adding riders, or purchasing umbrella insurance. Knowing your options allows for flexibility in response to changing circumstances.

Best Practices for Policy Limit Verification

To ensure effective policy limit verification, consider these best practices:

Review Policies Regularly: Conduct an annual review to confirm that your coverage still meets your needs.

Keep Records: Maintain detailed records of policy limits, endorsements, and communication with the insurer.

Consult a Professional: Insurance agents or brokers can provide guidance to ensure coverage aligns with risks and requirements.

Document Clarifications: If an insurer provides explanations or adjustments, document them for future reference.

Compare Policies: When shopping for insurance, compare limits across providers to ensure adequate coverage at competitive rates.

Conclusion

Policy limit verification is not just a routine exercise—it is a critical step in managing financial risk effectively. By asking the right questions and understanding the nuances of your insurance coverage, you can ensure that your policy provides adequate protection against potential losses.

From confirming per occurrence and aggregate limits to understanding sublimits, exclusions, and claims procedures, thorough verification prevents unpleasant surprises and promotes peace of mind.

Ultimately, the goal of insurance is to provide security and confidence. Taking the time to verify policy limits and clarify coverage details with your insurance company ensures that your safety net is both strong and reliable. Whether for personal insurance or commercial policies, these steps are indispensable in safeguarding your financial future.

Категории

Больше

How do I recover my lost Minecraft world? Losing a Minecraft world can be frustrating, but recovery may be possible call 1-888-653-7618 tollfree Minecraft support . depending on how the world was lost. If you’re playing on Minecraft Java Edition, start by checking the “saves” folder. Press Windows + R, type and press Enter. How do I recover my lost Minecraft world?...

From family vehicles and sports equipment to tools and storage, your garage floor works harder than most surfaces in your home. Unfortunately, bare concrete isn’t built to last under constant use, spills, and Oklahoma’s unpredictable weather. That’s why choosing a garage floor coating from Blue Shield Floor Coatings is one of the smartest upgrades you can make. Not only does...

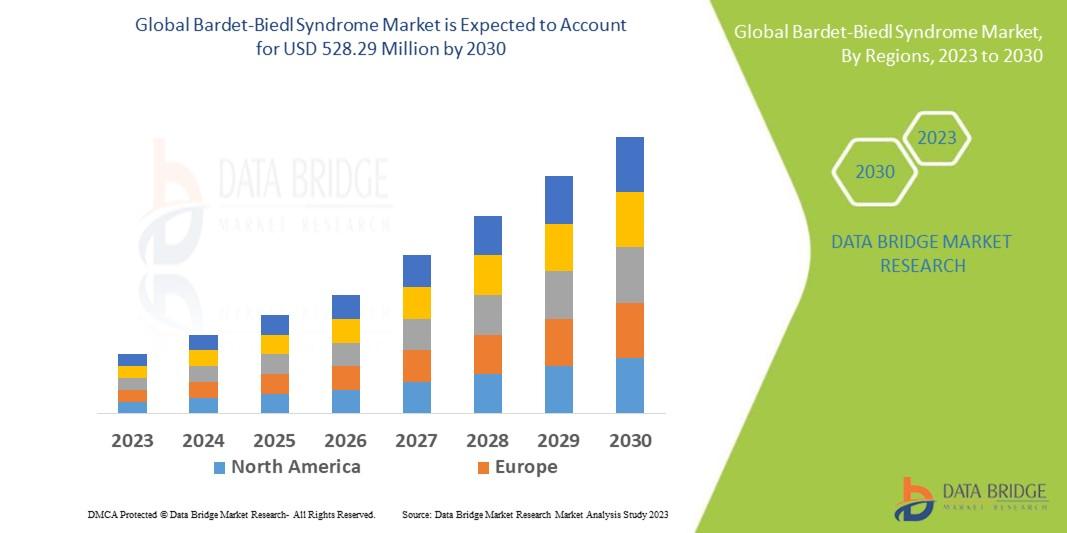

"Latest Insights on Executive Summary Bardet-Biedl Syndrome Market Share and Size CAGR Value Data Bridge Market Research analyzes that the global Bardet-Biedl syndrome market, which was USD 349.22 million in 2022, is likely to reach USD 528.29 million by 2030 and is expected to undergo a CAGR of 5.9% during the forecast period 2023 to 2030. Bardet-Biedl Syndrome...

本人確認不要オンラインカジノは、オンラインカジノ世界で最も目新しいトレンドです。本人確認不要オンラインカジノは本人 確認 不要 オンライン カジノオンラインカジノに参加するためにはあらゆる情報の提出を必要としない専門的なカジノプレイヤーを対象にしたサービスです。安全性と利便性の両立を実現するために、カジノ企業が発展しています。 遊雅堂における本人確認不要オンラインカジノ 遊雅堂は、日本円に対応したカジノゲームやスポーツベットを提供するカジノ企業です。那では、本人確認不要オンラインカジノを機能させることで、より多くのプレイヤーを привлекることができます。 カジノシークレットの本人確認不要オンラインカジノ カジノシークレットは、即出金可能なインスタントキャッシュバックを提供するカジノ企業です。それがカジノプレイヤーにとって魅力的な要素です。...

"Executive Summary Embolization Particle Market : The global embolization particle market size was valued at USD 2.40 billion in 2024 and is projected to reach USD 5.67 billion by 2032, with a CAGR of 11.32% during the forecast period of 2025 to 2032. This market report comprises of a chapter on the global market and allied companies with their profiles, which delivers essential data...