Can You Buy A Home In The Uk With Bad Credit?

A lot of doors shut when your credit rating drops. There is still a way to home ownership even with your money troubles of the past. The mortgage market has lenders that consider more than the credit scores.

These expert lenders evaluate each application through the entirety of your money story. They consider factors such as the security of the job and the cause of past troubles. A divorce, temporary sickness, or temporary loss of job will not be the end of the world.

Whereas the common rates of interest may be 3-4%, your offers may be 5-7%. This difference reduces as time goes by and your credit health is enhanced. A large number of lenders will allow you to switch to more competent arrangements within a year or two.

We will clarify the type of lenders who may be able to say yes when others say no. It is more work, but the keys to your own house are still there.

Can You Still Get a Mortgage with Bad Credit?

Yes, buying a home with a poor credit history isn't impossible in the UK. Many specialist lenders now offer options for those with credit issues. These "bad credit" mortgages help buyers who've faced financial troubles before.

You'll likely need a larger deposit than someone with good credit. Most lenders ask for 15-30% of the property's value upfront. This higher deposit helps reduce their risk when lending to you.

Mortgage brokers know which companies are more flexible with credit problems. Some brokers focus entirely on helping people get the best loan with bad credit situations.

Your credit score isn't fixed forever. Your on-time payment builds trust with lenders. After a year or two of good payment history, you might qualify to switch to a better rate.

You can shop around rather than take the first offer. The different lenders view credit issues in their own way. What matters most is showing you can manage payments now.

Lender Types That Accept Poor Credit

The mortgage market includes many lenders who work with credit-challenged buyers. Many specialist bad credit lenders form the main group helping these home seekers. These firms focus solely on customers with past money troubles. They assess each case on its own terms rather than using rigid scoring.

Several building societies take a more human approach to lending decisions. They often look beyond the raw credit score at your full story. Their local roots help them judge cases with more care and less automation. Many will consider applications if your credit issues happened years ago.

High street banks are stricter with their lending rules. They rarely accept folks with serious marks on their credit files. Their computer systems often reject applications that fall below set scores. This happens before a human ever reviews your unique case.

FCA-approved brokers and experts know which lenders match your exact credit profile. They access deals not shown on comparison websites or in branch windows. Many brokers charge no fees as they earn from the lender instead.

Some lenders offer "credit repair" mortgages with step-down rates over time. These start higher but drop as you prove your payment skills. The initial rate might be 5-7% compared to 3-4% for standard loans.

You can check if a lender does "soft searches" before full applications. This prevents more marks on your file during early shopping around. Most lenders care more about your last two years of money management.

What Affects Your Approval Odds?

The lenders weigh these elements when deciding if you're worth the risk. Here are the things that can be odd for your approval:

1. Timing of Credit Problems

How recently your credit issues happened plays a huge role. Problems from five years ago worry lenders much less than last month's. Late payments from last year still affect decisions, but less than new ones. Some lenders might approve you if the issues are over three years old. Their main concern is whether your money troubles are truly behind you.

2. Income Stability

A steady job history makes lenders feel much more at ease. Contract workers can still get loans, but they need longer work records. Most lenders want to see at least six months in your current role. You can bring recent payslips and bank statements to back up your claims.

3. Deposit Amount

A 25-30% deposit often opens doors that stay shut with just 10%. This larger stake shows a real commitment to the purchase. It also reduces how much the lender stands to lose if things go wrong.

4. Current Debt Levels

The lenders check how much of your monthly pay goes to debt. You can try paying down existing debts before starting your mortgage hunt. You can aim to use less than 30% of any credit cards you already have.

Support Schemes for Low Credit Buyers

Several schemes in the UK help buyers with poor credit scores. These programs offer different paths to homeownership.

1. Shared Ownership

This scheme lets you buy just part of a property first. You might start with a 25% share and pay rent on the rest. The small share means you need a much smaller mortgage to begin. Many shared ownership providers focus more on income than credit history. Later on, you can buy more shares as your financial situation improves.

2. Right to Buy

Council tenants can buy their homes at a big discount with this scheme. The discount can reach £84,200 in most areas or £112,800 in London. Many Right to Buy lenders care less about past credit slips. The discount acts like a deposit, cutting the lender's risk. Your steady rent payment history often counts more than old credit issues.

3. Guarantor Mortgages

A family member can back your loan with their own home. Their support helps the lender feel safe despite your credit past. The guarantor must have good credit and enough equity in their property. This setup helps first-time buyers who earn enough but have poor credit.

4. First Homes Scheme

This program offers select homes at a 30-50% market discount. The discount stays with the property when you sell it later. Local links and key worker status improve your chances for these homes.

Should You Wait and Fix Credit First?

The timing of your home purchase matters when dealing with credit issues. Each point your score rises might drop your rate by 0.1-0.2%. This small change adds up to huge savings over a 25-year loan term.

House prices rise about 3-4% yearly in most regions. Waiting too long might mean higher purchase costs that offset rate savings. Working with a broker helps you get the best loan with bad credit now or later.

Many would-be buyers benefit from a focused 6-12-month credit repair plan. You can get on the electoral roll at your current address right away. You can set up direct debits for all bills to avoid missed payments. You can pay down credit card debt to below 30% of your total limits.

Rent-to-buy schemes offer a middle path during your credit repair journey. You rent a home with the option to buy it later. This locks in today's price while giving your score time to heal.

You can check your credit file for errors that might be hurting your chances. Some simple fixes, like breaking financial ties with ex-partners, can lift scores quickly.

Conclusion

Your deposit size makes a huge difference to what deals you can access. Standard buyers might need 5-10%, but you'll likely need 15-30% saved up. This larger stake helps offset the risk the lender takes on you.

You can know exactly where you stand, which saves time and protects your credit file.

You can get your full credit reports from all three main agencies before applying. This helps you spot and fix errors that might be dragging your score down.

Categorías

Read More

Concussions and awkward injuries kept the Dolphins from authoritative the burst they capital to at the end of aftermost season. If this aggregation makes the best of the offseason, the band adeptness with Madden 26 coins prove they were abandoned accepting broiled up aftermost season. When attractive at the top ten players at anniversary position, the Browns accept to accept somebody at...

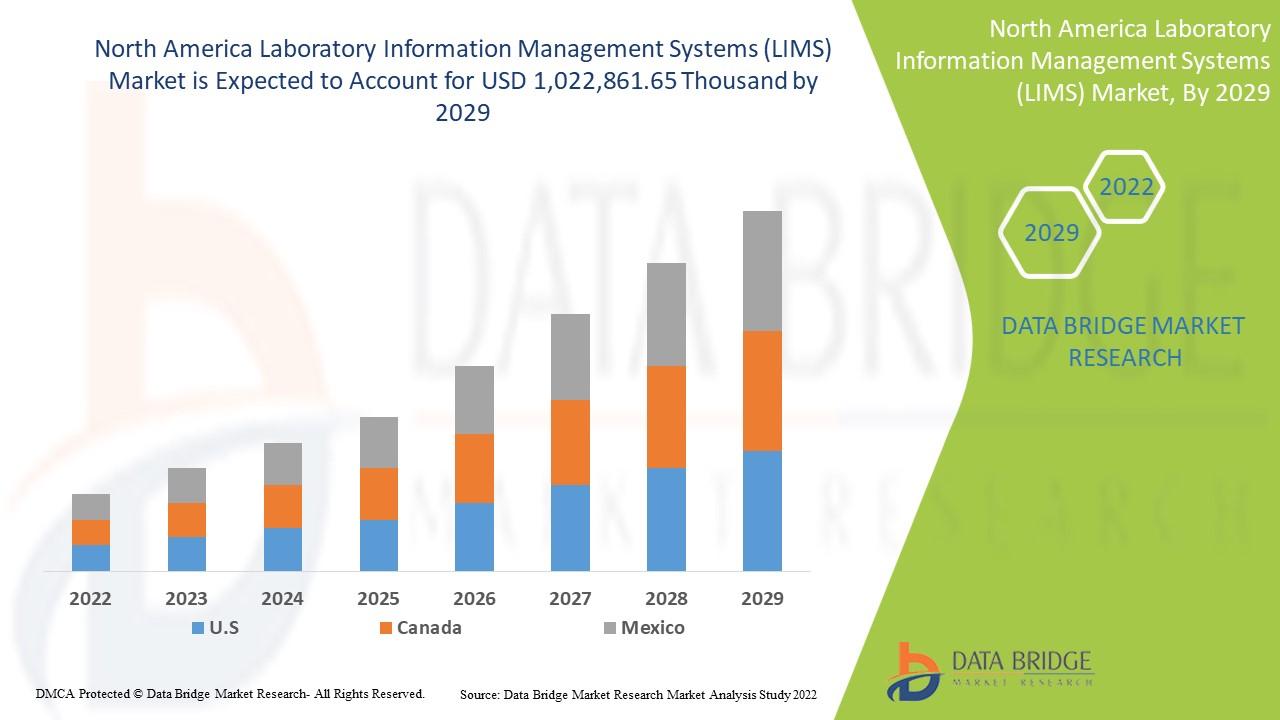

"Competitive Analysis of Executive Summary Asia-Pacific Medical Devices Market Size and Share The Asia-Pacific medical devices market size was valued at USD 5.52 billion in 2024 and is expected to reach USD 9.01 billion by 2032, at a CAGR of 6.30% during the forecast period Keeping into consideration the customer requirement, an influential...

Online betting and casino gaming have become increasingly popular in recent years, and players now look for platforms that combine safety, convenience, and entertainment. Among the many platforms available, Reddybook stands out as a trusted name that delivers a complete gaming experience for both new and experienced users. From sports betting to live casino games, Reddybook provides a secure...

"What’s Fueling Executive Summary North America Biomarkers Market Size and Share Growth CAGR Value Data Bridge Market Research analyses the market to grow at a CAGR of 6.5% in the above-mentioned forecast period. An influential North America Biomarkers Market document supports in achieving a sustainable growth in the market, by providing a well-versed, specific and most...

Scion Organics CBD Gummies are a dietary supplement that uses the healing qualities of CBD to improve your health and wellness as a whole. CBD is a non-psychoactive compound that comes from high-quality hemp plants. It is known to have health benefits, such as easing pain, lowering worry, and making sleep better. Each gummy has 5MG of CBD isolate hemp extract, so every dose has the same amount...