Struggling to Get a Loan on ₹25,000 Salary? Try These Tips

Financial needs often arise unexpectedly—be it medical emergencies, education, weddings, or simply consolidating debt. For salaried individuals earning ₹25,000 per month, securing a personal loan can feel like an uphill task.

Lenders usually prefer borrowers with higher incomes, as it signals better repayment capacity. However, don’t lose hope. Earning ₹25,000 doesn't automatically disqualify you from getting a loan—it just means you need to be a little more strategic.

If you're struggling to get a personal loan on 25,000 salary, here are practical, proven tips to improve your chances of approval:

1. Know the Minimum Eligibility Criteria

Every lender—be it a bank, NBFC, or digital lending platform—has its own eligibility guidelines. However, most have a minimum income requirement, which can vary by city. For instance, in metro cities, the cut-off may be ₹25,000, while in smaller towns it might be ₹15,000–₹20,000.

Before applying, check:

-

Age: Usually 21–60 years

-

Employment type: Salaried with at least 6 months–1 year in the current job

-

Salary credit: Must be credited to a bank account (not cash-in-hand)

-

Location: Some lenders cater only to specific cities or regions

Applying without meeting these criteria can lead to rejection and a negative impact on your credit score.

2. Maintain a Good Credit Score

Your credit score (typically 300–900) is one of the most important factors lenders consider. A score above 700 is generally considered good.

To improve your credit score:

-

Pay your credit card bills and EMIs on time

-

Avoid multiple loan applications in a short period

-

Keep your credit utilization ratio low (ideally under 30%)

If you have no credit history, consider starting with a secured credit card or small consumer durable loan to build your score.

3. Opt for a Lower Loan Amount

With a ₹25,000 monthly salary, you might not be eligible for a high loan amount. Lenders evaluate your repayment capacity, and ideally, your EMI should not exceed 30–40% of your monthly income. That means your EMI should ideally be under ₹7,500–₹10,000.

Instead of applying for ₹2–3 lakhs, start small. Ask for ₹50,000–₹1 lakh if that meets your needs. Lower loan amounts have higher chances of approval for low-income borrowers.

4. Choose a Longer Loan Tenure

A longer repayment period means smaller EMIs, which makes the loan more manageable on a ₹25,000 salary. Although you may end up paying more interest overall, this strategy increases your chances of approval.

For example:

-

A ₹1 lakh loan for 12 months may require an EMI of ₹9,000+

-

The same loan over 24–36 months could drop the EMI to ₹3,000–₹5,000

Always use a personal loan EMI calculator to find the ideal balance between tenure and monthly outflow.

5. Add a Co-Applicant or Guarantor

If your income alone doesn’t meet the eligibility criteria, consider applying with a co-applicant—like a spouse or parent with a stable income and good credit history. This significantly improves your chances of loan approval.

Some lenders may also allow a loan guarantor, who agrees to repay if you default. Be sure your co-applicant or guarantor is financially sound and understands their obligations.

6. Apply with the Right Lender

Not all lenders are the same. While some banks have stricter eligibility norms, many NBFCs (Non-Banking Financial Companies) and digital lending platforms are more flexible and cater to lower-income borrowers.

Look for lenders that:

-

Offer small-ticket personal loans

-

Have minimal documentation

-

Are open to low-income or first-time borrowers

Some fintech platforms even approve loans based on alternative credit scoring, using utility bill payments, employment stability, and other behavioral data.

7. Keep Your Documents Ready

Having your documents in order speeds up the approval process. Typically, you’ll need:

-

PAN card and Aadhaar card

-

Salary slips (last 3–6 months)

-

Bank statements (last 3–6 months)

-

Employment certificate or ID

-

Address proof

Make sure your salary is credited via bank transfer—not cash—as lenders prefer verifiable income.

8. Don’t Apply to Too Many Lenders at Once

Each loan application triggers a hard inquiry on your credit report. Too many applications in a short span make you look credit-hungry and can lower your credit score.

Instead, use pre-approval tools or check your eligibility on loan aggregator websites. These do soft inquiries that don’t impact your score and give you a fair idea of where you stand.

Final Thoughts

Getting a personal loan on a ₹25,000 salary isn’t impossible—it just requires the right approach. Focus on building your credit profile, borrow within your means, and choose lenders that understand the needs of low-income salaried individuals. With the right strategy, you can get the funds you need without overburdening yourself.

Kategoriler

Read More

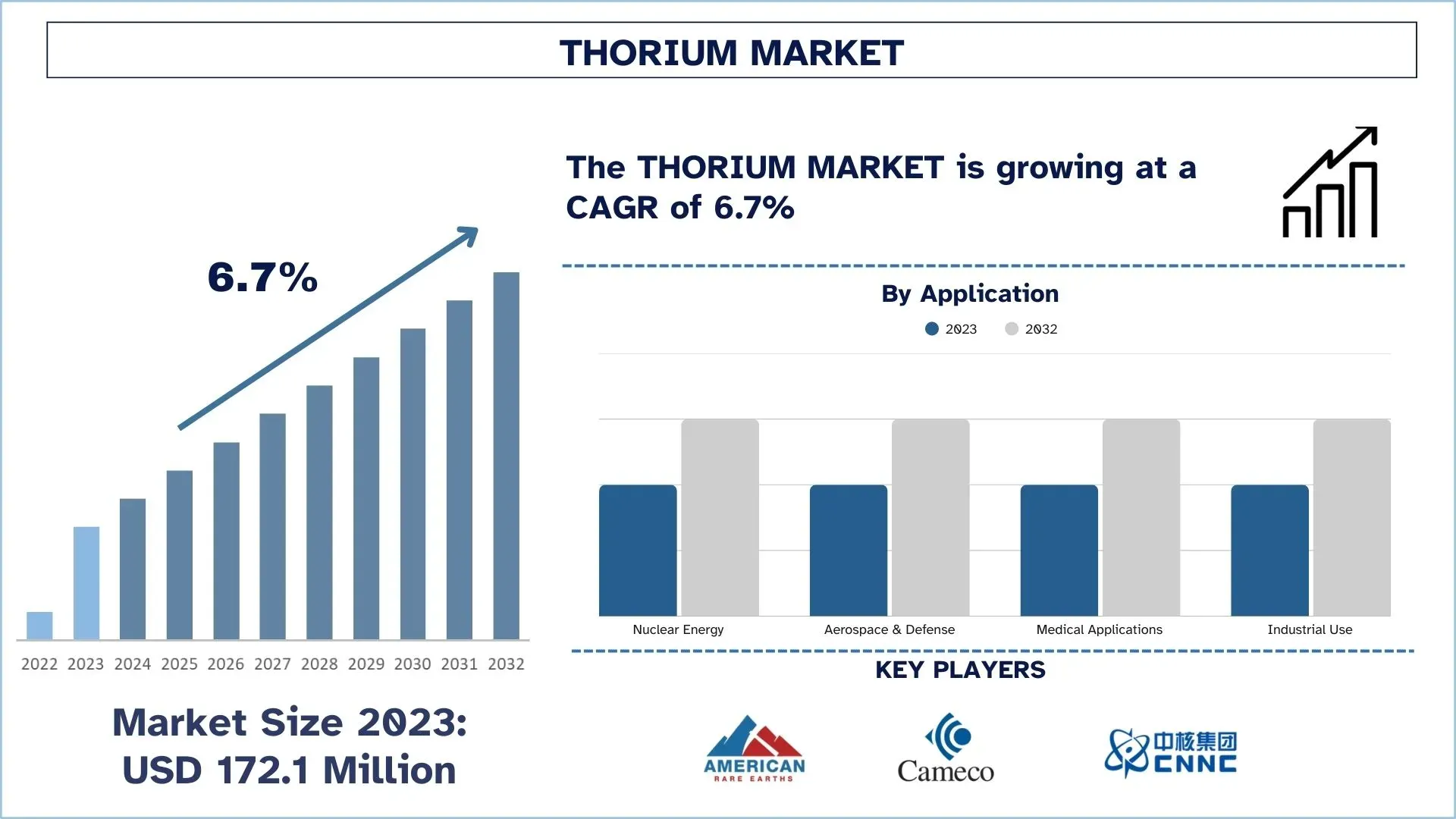

According to a new report by UnivDatos, the Thorium Market is expected to reach USD 308.5 million in 2032 by growing at a CAGR of 6.7%. The nuclear energy business favors thorium due to its higher efficiency while creating less radioactive waste and providing better safety than uranium. Advanced reactor technologies need thorium, which is extracted mainly from three types of sites: monazite...

There's nothing better than enjoying the company of VIP Abu Dhabi Escort most beautiful and stunning beauties. Yes, we're talking about Escort Abu Dhabi VIP! Abu Dhabi escorts are undoubtedly the best! They are beautiful, talented, extremely attractive, and exceptionally creative in their performance. And you know what's the best part? You can hire these beautiful girls from our exemplary Abu...

Are you planning a party and looking for ways to make it extra special? Consider renting a water slide for your next event! Water slide rentals can provide endless fun and entertainment for guests of all ages. In this article, we will discuss the top benefits of choosing water slide rentals for your next party. Affordable Entertainment Option Water slide rentals are a cost-effective way...

In the rapidly evolving world of home automation and security, electric gates are fast becoming essential features for residential and commercial properties. Homeowners and business owners alike in Perth are now prioritizing security and convenience by investing in Electric Sliding Gates Perth and Electric Solar Gates Perth. One name that consistently stands out in this industry is Western...

Travelers heading from Disneyland Paris to Charles de Gaulle Airport often look for a hassle-free way to reach their flights promptly. Using a shuttle from Disneyland to CDG ensures a direct, safe, and comfortable ride, bypassing the challenges of public transportation. Modern shuttle services cater to tourists, offering spacious vehicles, luggage assistance, and friendly drivers who prioritize...