The Impact of LDS Mission Returns on Young Driver Insurance Costs in Salt Lake City

Introduction: When Faith and Finances Intersect

For many families in Salt Lake City, serving a mission for the Church of Jesus Christ of Latter-day Saints is a sacred rite of passage. But what often gets overlooked is how this two-year break can impact the cost and structure of auto insurance when a young driver returns home.

Teen drivers and those in their early 20s already face some of the highest insurance premiums due to inexperience and perceived risk. Add a two-year hiatus from driving—and insurance coverage—and the return to the road can bring new financial surprises. In this post, we explore how LDS mission returns affect young driver insurance in Salt Lake City, and what steps families can take to minimize costs and avoid coverage gaps.

Why Insurance Rates for Young Drivers Are Already High

Before we dive into how missions affect rates, it helps to understand why young drivers (typically ages 16–25) pay more in the first place:

-

Higher accident statistics: National data shows young drivers are involved in more accidents per mile than older drivers.

-

Limited driving history: Insurers have less to go on when calculating risk.

-

Increased claim frequency and severity: Even minor incidents can lead to higher payouts.

In Utah, where many young people take time off for missionary service, this profile becomes more complex—and often misunderstood by insurance providers that don’t specialize in the region's unique demographic trends.

Scenario 1: Keeping Coverage Active During a Mission

Some parents opt to leave their missionary child listed on the family auto policy throughout their mission. On the surface, this might seem wasteful—they're not driving, so why pay? But there are a few pros:

-

No lapse in coverage history, which can help keep premiums lower upon return.

-

Some companies offer "non-driver" discounts or allow temporary rate adjustments if the insured isn’t driving but remains on the policy.

-

Maintains eligibility for multi-vehicle or multi-driver discounts, depending on the carrier.

However, this method doesn’t come cheap. Most standard policies won’t drop rates significantly just because a driver isn’t currently behind the wheel. That’s where communication with your insurance provider is key.

Scenario 2: Removing the Missionary from the Policy

The more popular strategy is to remove the young driver from the policy while they are away on their mission. This typically saves families hundreds—sometimes thousands—over two years.

But there’s a catch: insurers may view this as a lapse in coverage.

Even though the lapse was voluntary and for a good reason, some insurance algorithms don’t distinguish between a gap due to a religious mission and one due to irresponsibility or inability to maintain insurance. As a result, returning missionaries may be quoted higher rates when reapplying for coverage.

Fortunately, many local Utah insurance providers understand this situation and don’t penalize for mission-related lapses—but it’s not universal.

Pro Tip: Ask your insurer in advance how they treat missionary coverage gaps, and get the answer in writing.

This ensures a smoother re-entry when the missionary returns home.

Documentation That Can Help

To support a smooth insurance reinstatement after a mission, keep these documents handy:

-

Official mission call and release letter

-

Dates of service (start and end)

-

Signed letter of explanation if switching to a new provider

-

Parent's or guardian’s insurance history, especially if the young driver was previously listed on a family policy

Many agents in Utah are familiar with this process and can help submit these documents to underwriting departments to ensure favorable rate consideration.

How Returning Missionaries Can Shop Smart

Upon return, many young drivers are ready to jump back into daily life—school, work, and driving. Here's how to secure young driver insurance in Salt Lake City without overspending:

1. Compare Multiple Providers

Don’t settle for the first quote. National brands may penalize coverage gaps, but many local and regional providers understand LDS mission dynamics and can offer lower rates.

You can explore auto insurance quotes Salt Lake City to find plans tailored to local lifestyles and driving patterns.

2. Consider a New Policy as an "Occasional Driver"

If the returned missionary isn’t driving full-time—perhaps they’re on campus at the U of U or using public transit—they may qualify for an occasional driver discount on a family plan.

3. Look into Telematics Programs

Many insurers now offer usage-based insurance, where a device or app monitors driving behavior and mileage. Safe driving and low mileage can lead to significant discounts—perfect for cautious post-mission drivers.

4. Ask About "Good Student" Discounts

If the returning missionary is now in college and maintaining a strong GPA, that could knock up to 15% off the premium. Combine that with safe driving and a clean record, and the savings start stacking.

Avoiding Common Pitfalls

Here are a few mistakes families often make when it comes to post-mission auto insurance:

-

Failing to notify the insurer about the mission in advance

-

Assuming all insurers will honor a missionary gap the same way

-

Waiting until the driver returns to start the reinstatement process

-

Choosing a national provider unfamiliar with Utah-specific practices

Final Thoughts: Plan Ahead to Save Later

Whether you're a parent preparing to send off a missionary or a young adult just returning, it pays to think ahead. The decisions you make today—keeping coverage, pausing it smartly, or switching providers—can affect insurance premiums for years to come.

The best way to get affordable young driver insurance in Salt Lake City after a mission is to work with agents who understand LDS culture, Utah driving patterns, and insurance underwriting. A mission shouldn't be a financial setback when it comes to car insurance—and with the right preparation, it won’t be.

Categorii

Citeste mai mult

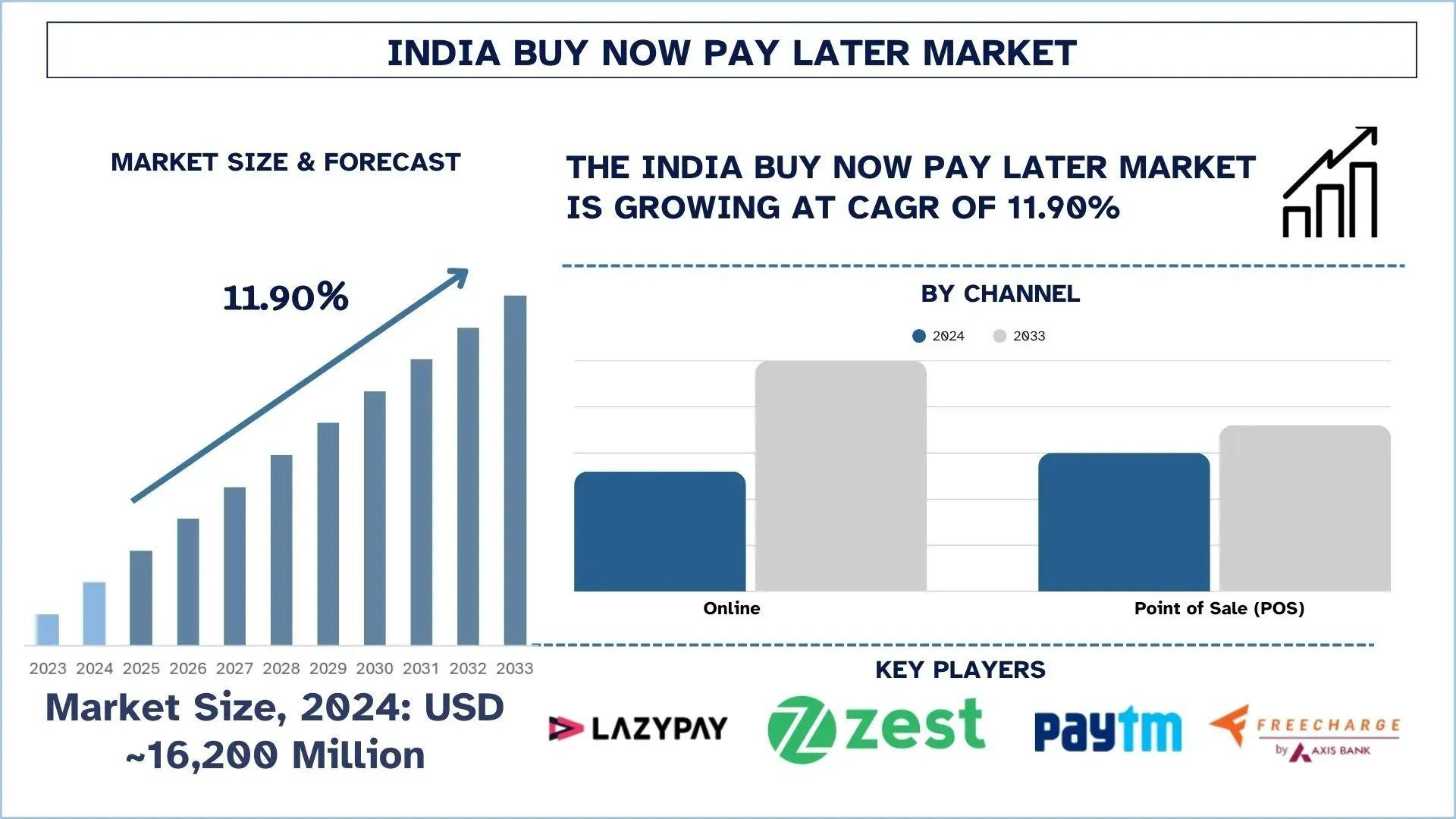

According to the UnivDatos, are rising e-commerce penetration, increasing digital payment adoption via UPI & wallets, millennial and Gen Z preference for instant credit, lack of access to traditional credit instruments (e.g., credit cards), rapid smartphone and internet penetration in Tier II & III cities, growing demand for contactless and flexible payment options drive the India Buy...

"Executive Summary Grease Market : Data Bridge Market Research analyses that the grease market was valued at USD 5.45 billion in 2021 and is expected to reach USD 6.78 billion by 2029, registering a CAGR of 2.77% during the forecast period of 2022 to 2029. For a powerful business growth, companies must take up market research report service which has become quite vital in this rapidly...

Table of Contents Introduction What is ISO 9001 Quality Management? Why Quality Matters for Business Success Core Principles of ISO 9001 How ISO 9001 Elevates Product and Service Quality Standardized Processes for Consistency Customer-Centric Approach Continuous Improvement Culture Key Benefits of ISO 9001 Quality Management Improved Product and Service Quality Increased...

Grassfed Meat Market, By Product Type (Raw Meat, Processed Meat), Nature (Organic, Conventional), Animal Type (Cow, Bison, Lamb, Goat), Sales Channel (Direct Sales, Retail Sales), End User (HoReCa, Food Processing, Household) – Industry Trends and Forecast to 2030. Data Bridge Market Research analyses that the grassfed meat market is expected to reach USD 20.57 million by 2030, which is...

Presentation to Raspberry Hills Raspberry Hills has rapidly gotten to be a go-to title for those looking for in vogue and solid attire. The brand Raspberry Hills offers a one-of-a-kind mix of present-day mold and viable wearability, making it prevalent among different groups of consumers. Known for its quality and attention to detail, Raspberry Hills has carved a specialty in the design...