Halogen Floodlights Market Set to Reach USD 2.6 Billion by 2030 Amid Steady Demand from Construction, Municipal, and Niche Applications

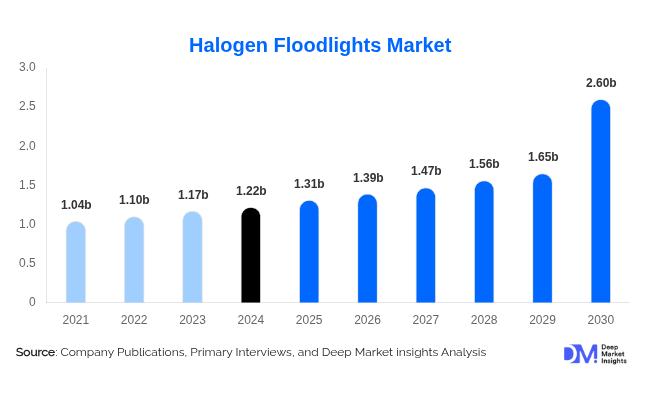

According to Deep Market Insights, " The global halogen floodlights market, valued at USD 1.22 billion in 2024, is projected to expand from USD 1.31 billion in 2025 to USD 2.6 billion by 2030, reflecting a compound annual growth rate (CAGR) of 6% during the forecast period (2025–2030). Despite the widespread transition to LED and smart lighting technologies, halogen floodlights continue to demonstrate relevance in cost-sensitive and specialized applications across multiple regions.

Market Dynamics

Dominant Wattage Segment:

The 150W–500W segment remains the most widely adopted, particularly in commercial and municipal settings. These systems balance affordability with sufficient illumination, making them suitable for street lighting, parking lots, retail exteriors, and mid-sized venues.

Application Hotspots:

Construction and industrial sites lead demand, driven by halogen’s durability, affordability, and high lumen output. Municipal bodies also sustain procurement in rural and budget-constrained areas, ensuring stable baseline demand.

Regional Overview:

-

Asia Pacific leads the market, supported by infrastructure projects and rural electrification in India, Indonesia, and Vietnam.

-

North America maintains moderate demand, with rural municipalities relying on halogens due to phased LED transition and budget limitations.

-

Europe faces contraction due to energy efficiency regulations but sustains niche use in theaters and stage lighting where halogen brightness and color rendering remain preferred.

-

Middle East & Africa show continued uptake in construction, hospitality, and event lighting, particularly in semi-urban regions.

-

Latin America sustains demand through municipal infrastructure, outdoor security, and sporting facilities, with affordability driving sales across hardware and retail outlets.

Market Drivers

-

Affordability and Lumen Output: Halogen floodlights remain a cost-effective choice for users seeking immediate brightness and minimal upfront investment. Their warm white light, simple installation, and compatibility with legacy systems support continued adoption.

-

Specialized Applications: Superior color rendering and instant illumination make halogen floodlights indispensable in film studios, theatres, heritage architecture, and high-precision industrial environments.

-

Durability and Voltage Tolerance: Halogen systems perform reliably in rugged conditions, making them suitable for construction zones, mining operations, and regions with unstable power grids.

Restraining Factors

-

High Initial Costs of Alternatives: Advanced LED and smart systems demand two to three times the upfront investment of halogens, delaying adoption in cost-sensitive regions.

-

Risk of Obsolescence: With manufacturers prioritizing R&D in LEDs and solar-powered systems, halogen units face declining availability of parts and regulatory restrictions in several markets.

Opportunities

-

Smart Cities and Infrastructure: Integration of lighting with urban platforms, as demonstrated in Barcelona’s Smart Lighting initiative, presents opportunities for hybrid halogen-to-LED retrofit projects.

-

Niche Market Growth: Applications in agriculture, aviation hangars, and explosion-proof zones continue to provide resilience against market decline.

Competitive Landscape

The halogen floodlights market remains competitive, with companies sustaining demand through targeted innovations and legacy system compatibility.

-

GE Lighting (a Savant Company): In February 2025, launched the “HalogenPro ToughSeries,” designed for construction and mining, featuring reinforced glass and metal housings for durability.

-

OSRAM GmbH: In March 2025, introduced the “VisualStar” halogen floodlight series tailored for studio and broadcast environments with high CRI and uniform light distribution.

-

STEINEL: In January 2025, unveiled its XLED Professional 5 LED floodlight series with adaptive sensors and OTA firmware support, marking continued transition efforts.

Other key players include NORDEX, Nordic Lights, STAHL, Rohrlux, RS Pro, Schreder Group GIE, SIRENA, SMP Electronics, STEINEL, Vision X Europe, WISKA Hoppmann GmbH, Wolf Safety Lamp Company, and Yaham Optoelectronics Co., Ltd.

Outlook

While LEDs and smart lighting dominate growth narratives, halogen floodlights are expected to maintain a resilient market share through 2030 in construction, municipal, and niche professional environments. Their cost-effectiveness, reliable performance, and compatibility with legacy infrastructure underpin a stable demand curve, particularly in developing economies and specialized industries.

Catégories

Lire la suite

ในโลกปัจจุบันที่ความเร็วกลายเป็นส่วนหนึ่งของชีวิตประจำวัน หลายคนอาจรู้สึกว่าการหาความรักหรือความสัมพันธ์ที่จริงใจนั้นยากขึ้น แต่ด้วยเทคโนโลยีและแพลตฟอร์มที่เข้าใจผู้ใช้จริงอย่าง Fiwfan ทุกอย่างก็ง่ายและมีความหมายมากขึ้น Fiwfan ไม่ใช่แค่แอปหาคู่ธรรมดา แต่มันคือพื้นที่สำหรับคนที่ต้องการ "ความสัมพันธ์ที่แท้จริง" ไม่ว่าจะเป็นความรัก มิตรภาพ หรือการรู้จักใครบางคนที่เข้าใจเราในแบบที่เราเป็นจริงๆ...

Sonam Basu: If you want blonde escorts service in Mumbai or nearby Mumbai. We offer the blonde call girls in Mumbai and blonde known for their beauty. he desires for sex will only be pleased, if your blonde escort and call girls service girls Mumbai escort and call girl can fit character, flavour and choices. Hence, while choosing the escort and call girls, it is important that you...

Executive Summary Flexible Pipe Market : The Global Flexible Pipe Market was valued at USD 10.21 Billion in 2024 and is expected to reach USD 32.3 billion by 2032, During the forecast period of 2025 to 2032 the Market is likely to grow at a CAGR of 4.4%, primarily driven by the increasing offshore oil & gas exploration spending on a global level. The...

In today’s competitive market, packaging plays a vital role not just in protecting the product, but also in branding and customer perception. Among the various packaging options, printed corrugated packaging stands out for its durability, eco-friendliness, and customizability. If you're a business owner or retailer looking for a Corrugated Packaging Box Wholesaler in India, this article...

"Executive Summary Middle East and Africa Retort Packaging Market : CAGR Value Data Bridge Market Research analyses that the Retort packaging market is expected to reach the value of USD 490.23 million by 2029, at a CAGR of 4.6% during the forecast period. Myriad of scopes are carefully evaluated through this Middle East and Africa Retort Packaging Market report which range from...