Interest Rate for Personal Loan on 20000 Salary: What You Need to Know

Personal loans are a popular financial solution for individuals who need quick access to funds—whether it’s for a medical emergency, home renovation, wedding expenses, education, or travel plans. If your monthly income is ₹20,000, you might be curious about your eligibility and the interest rates available for a personal loan on 20000 salary. Understanding how lenders assess applicants in this income bracket can help you make an informed borrowing decision.

Are You Eligible for a Personal Loan on ₹20,000 Salary?

Most banks and non-banking financial companies (NBFCs) have a minimum income requirement to approve personal loans. Generally, ₹15,000–₹20,000 per month is considered the minimum threshold in smaller cities, while the requirement might be slightly higher in metro areas.

So yes, if you earn ₹20,000 per month, you can be eligible for a personal loan, provided you meet other conditions like:

-

Good credit score (usually 650+)

-

Stable employment (minimum 6 months with the current employer)

-

Low existing debt burden

-

Age between 21 and 60 years

Interest Rate on Personal Loans for ₹20,000 Salary

The interest rate offered on a personal loan can vary depending on several factors:

-

Your credit score

-

Employer reputation

-

Location (metro vs. non-metro)

-

Loan tenure and amount

-

Lender’s internal policies

Typically, interest rates for personal loans in India range from 10% to 26% per annum. However, for someone earning ₹20,000 per month, the interest rate might lean toward the higher end of the spectrum.

Here’s what you might expect:

|

Credit Score |

Approx. Interest Rate |

|

750+ |

12% – 16% |

|

650–749 |

16% – 22% |

|

Below 650 |

22% – 26% (or rejection) |

Example: Loan Offer for ₹20,000 Salary

Let’s say you are offered a personal loan of ₹1,00,000 for 3 years at an interest rate of 18% p.a. Your EMI would be approximately ₹3,615. Considering your income, this EMI is close to 18% of your monthly salary, which is within acceptable limits for most lenders (who usually prefer the EMI-to-income ratio to stay under 40%).

How to Get the Best Interest Rate?

Here are some tips to help you secure a lower interest rate on your personal loan:

-

Improve your credit score: A score above 750 increases your bargaining power.

-

Apply with a reputed employer: Employees of MNCs or government organizations often get better terms.

-

Keep your debt low: The lower your existing EMIs, the better your chances.

-

Compare lenders: Use online tools or aggregators to find the best deals.

Final Thoughts

While earning ₹20,000 a month may limit your loan amount and increase your interest rate slightly, many lenders still offer personal loans in this income bracket. Focus on maintaining a good credit score, managing your existing debts, and applying through trusted financial platforms.

Categories

Read More

Warren Lotas || Warren Lotas Clothing || Official Store Warren Lotas world of streetwear, very few names carry the same mix of rebellion, controversy, and cult-like following as . His clothing line has carved out a unique space in the fashion industry by blending underground aesthetics, countercultural symbolism, and unapologetic boldness. Known for his dark graphics, skulls, flames,...

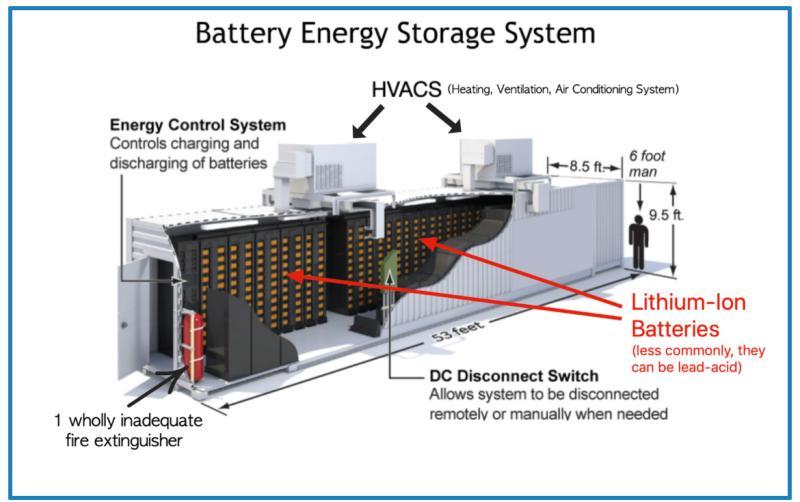

Lithium-Ion Battery Energy Storage System Market size was valued at USD 17.47 Billion in 2024 and the total Lithium-Ion Battery Energy Storage System Market is expected to grow at a CAGR of 5.45% from 2025 to 2032, reaching nearly USD 26.71 Billion..... Market Overview The global energy landscape is undergoing a transformative shift, with lithium-ion battery energy storage systems (BESS)...

When planning a group trip, whether for a corporate event, a school outing, or a family gathering, transportation becomes a key factor to consider. Comfort, cost-effectiveness, and efficiency are top priorities, especially when you're managing a large group. A 70-seater coach hire offers a perfect solution, catering to both large and medium-sized groups, ensuring everyone travels together...

StaminUP Testosterone Capsules Germany – In der heutigen schnelllebigen Welt stehen viele Männer vor Herausforderungen im Zusammenhang mit ihrer sexuellen Gesundheit. Faktoren wie Stress, Alter und Lebensstil können die männliche Leistungsfähigkeit und Vitalität beeinträchtigen. Fortschritte in Wissenschaft und Technologie haben jedoch zur Entwicklung...

"Executive Summary Azelaic Acid Manufacturing for Industrial Use Market : The global azelaic acid manufacturing for industrial use market size was valued at USD 172.50 billion in 2024 and is projected to reach USD 266.74 billion by 2032, with a CAGR of 5.6% during the forecast period of 2025 to 2032. The top notch Azelaic Acid Manufacturing for Industrial Use Market report...