V2X Cybersecurity Market Segment: Solutions, Services, and Application Areas

The V2X Cybersecurity Market Segment can be divided by security type, application, communication mode, and region. By security type, the market includes network security, application security, endpoint security, and cloud security, with network security leading due to its role in preventing unauthorized access. By application, the market serves passenger vehicles, commercial vehicles, and infrastructure, with passenger cars dominating adoption. Communication modes include vehicle-to-vehicle (V2V), vehicle-to-infrastructure (V2I), vehicle-to-grid (V2G), and others, with V2V and V2I being the most widely deployed.

Regionally, North America and Europe hold dominant shares owing to advanced mobility ecosystems and strong regulations, while Asia-Pacific shows high potential due to rapid smart city developments. This segmentation highlights the broad application of V2X cybersecurity across the connected mobility ecosystem. With varying needs across segments, providers are tailoring solutions to ensure robust, scalable, and future-ready protection for both vehicles and infrastructure.

As smart vehicles, autonomous driving systems, and connected infrastructure become increasingly integrated, vehicle-to-everything (V2X) communication underpins the next generation of mobility. V2X—an umbrella term encompassing vehicle-to-vehicle (V2V), vehicle-to-infrastructure (V2I), vehicle-to-pedestrian (V2P), and vehicle-to-network (V2N) connectivity—is critical for optimizing traffic flows, improving safety, reducing emissions, and enabling autonomous operation. However, as cars and infrastructure become hyper-connected, they also become vulnerable to cyber threats. The V2X cybersecurity market has emerged to safeguard this evolving ecosystem, offering hardware, software, and service solutions that ensure safety, privacy, and resilience—transforming cyber-risk into managed risk for future mobility.

Understanding the V2X Cybersecurity Landscape

V2X cybersecurity covers a wide spectrum of protections: secure communication protocols, message authentication, intrusion detection systems (IDS), anomaly monitoring, identity and certificate management, and firmware-over-the-air (FOTA) update security. Unlike traditional automotive cybersecurity, which focuses mainly on in-vehicle networks (CAN, Ethernet, etc.), V2X adds a broader attack surface—wireless links to external systems, roadside units, traffic infrastructure, cloud platforms, and mobile devices.

This creates complex threat models: man-in-the-middle attacks intercepting safety messages, spoofed infrastructure signals causing accidents, denial-of-service attacks on communication channels, and privacy breaches through traffic data. The V2X cybersecurity market seeks to address these risks via a layered defense model—securing in-vehicle ECU software, hardening communication protocols (e.g., IEEE 1609.2 or ETSI ITS standards), enabling tamper-resistant hardware modules, and providing secure lifecycle management of connected vehicles.

Market Drivers

Several key forces are fueling growth in the V2X cybersecurity market:

- Autonomous and connected vehicle deployment: Advanced driver-assistance systems (ADAS) and increasing levels of vehicle autonomy depend on reliable data from V2X. To ensure safety, cybersecurity defenses must be in place from the ground up.

- Regulation and standardization: Regulators around the world are beginning to mandate cybersecurity requirements for connected and autonomous vehicles. For instance, UNECE WP.29 requires cybersecurity management systems in vehicle type approvals. Regional standards (like European Union/ETSI or U.S. NHTSA guidelines) are forming a baseline that automotive OEMs and suppliers must meet.

- High-profile hacking incidents: Demonstrations—such as remote vehicle hijacking, spoofed braking commands via wireless exploits, and false traffic alert injections—raise public awareness and compel industry investments in V2X resilience.

- Insurance and liability concerns: As liability shifts in semi-autonomous and autonomous driving environments, insurers and OEMs are demanding better assurance that V2X communications are robust and tamper-resistant.

- Urbanization and smart infrastructure: Smart city initiatives rely on connected infrastructure—traffic lights, pedestrian beacons, roadside sensors—and this increases the demand for secured V2I and V2N channels.

Market Segmentation

The V2X cybersecurity market can be segmented across several dimensions:

- By Solution Type:

- Communication Security: Protocol stack protection, encryption and authentication, PKI and certificate management, secure channel establishment.

- Intrusion Detection & Incident Response: On-board IDS, cloud-based anomaly detection, alert systems, forensic logging.

- Endpoint and OTA Protection: Secure boot, hardware security modules (HSMs), secure firmware updates, tamper detection.

- Managed and Consulting Services: Threat modeling, penetration testing, cybersecurity risk assessments, incident management.

- By Deployment Model:

- OEM-integrated Embedded Solutions: Pre-installed at the vehicle manufacturing stage.

- Aftermarket Security Services: Updates, security patches, and monitoring services provided post-sale.

- Infrastructure & Smart City Solutions: Security for V2I nodes, RSUs, traffic management systems, and connected infrastructure.

- By Industry Vertical:

- Passenger Vehicles: Addressed by OEM cybersecurity programs.

- Commercial Fleets: Supplying sectors like trucking, logistics, ride share, where secure connected services enable fleet safety and efficiency.

- Public Transport Infrastructure: Smart buses, rail crossing systems, and connected highways with V2I requirements.

Competitive Landscape

The V2X cybersecurity market is characterized by a mix of automotive players, cybersecurity specialists, and standards consortia:

- Automakers & Tier-1 Suppliers: OEMs like Ford, BMW, Toyota are building cybersecurity into connected platforms, while Tier-1s such as Continental, Bosch, and Denso develop embedded security modules and secure comms stacks.

- Dedicated Security Vendors: Companies like Karamba Security, Argus Cyber Security, NXP, and Harman (Samsung) offer automotive-grade IDS, secure hardware, or secure OTA platforms.

- Sensor and Communications Companies: Firms that produce DSRC or C-V2X modules, such as Qualcomm, Cohda Wireless, and Savari, often embed encryption and PKI features into their hardware.

- Consultancies and Testing Labs: Entities like UL, NCC Group, and TÜV Rheinland provide regulatory compliance services, penetration testing, and standard certification for V2X.

Regional Market Insights

- North America: Early adoption markets with growing deployment of V2X pilot projects (e.g., Michigan test corridors, smart city trials). With support from DOT and research agencies, cybersecurity is being integrated into urban testbeds.

- Europe: Strong regulatory push through UNECE mandates gives vehicle manufacturers a clear compliance roadmap. EU smart mobility frameworks encourage V2I security for city infrastructure rollouts.

- Asia-Pacific: China, Japan, and South Korea are investing heavily in connected vehicle infrastructure. Domestic OEMs are coupling V2X capabilities with cybersecurity-driven guardrails in national smart mobility projects.

- Rest of World: Emerging regions are expected to lag in V2X cybersecurity investments but will catch up as connected infrastructure expands and cost-effective solutions become available.

Challenges and Risks

Despite promising momentum, the V2X cybersecurity market faces challenges:

- Interoperability and Legacy Integration: Multiple communication protocols (DSRC, C-V2X) and older vehicle generations need seamless and secure integration, adding complexity.

- Cost Constraints: OEMs often work on tight margins. Integrating layered cybersecurity raises vehicle costs, and aftermarket consumers may resist paying for security add-ons.

- Rapidly Evolving Threat Landscape: V2X creates new threat vectors that evolve constantly, requiring adaptive and updatable security designs.

- Regulatory Fragmentation: Differing regional mandates and standards can complicate global OEM and Tier-1 compliance strategies.

- Liability Uncertainty: As vehicles become autonomous, attribution of fault in a cyber attack remains legally murky, affecting risk assessments and insurance pricing.

Opportunities Ahead

The V2X cybersecurity market offers significant growth potential through:

- Embedded security platforms: OEMs that integrate firmware-level protections, secure communications chips, and PKI from design stage will lead in compliance and competitive differentiation.

- Over-the-air (OTA) Security: Robust, secure OTA infrastructure to patch vulnerabilities in deployed vehicles remotely will become a core offering—preventing recall-heavy fixes.

- Managed Security Services for Fleets: Fleet operators can subscribe to real-time monitoring, threat alerts, and incident response services for connected vehicle fleets.

- Infrastructure Protection: Cities and infrastructure agencies investing in V2I and V2N solutions will need hardened, tamper-resistant endpoints and secure gateways.

- Cyber Insurance and Compliance Bundles: Insurance products tied to certified cyber-protected fleets, coupled with regulatory compliance certificates, will lower OEM and fleet adoption risk.

- Cross-domain Expertise: Providers combining cybersecurity competence with automotive systems knowledge—such as secure automotive cloud, telematics, or autonomous driving stacks—will have an integrated advantage.

Future Outlook

The V2X cybersecurity market is poised for steady growth as connected and autonomous vehicles become mainstream. The market will evolve from point solutions (e.g., secure comms chips) toward systemic, lifecycle-spanning platforms that cover embedded security, threat monitoring, OTA updates, and regulatory compliance. Multi-modal security (V2V, V2I, V2N, and V2P) will become a standard design baseline in future mobility.

By 2030, cybersecurity may represent a substantial portion of vehicle system spend—comparable to infotainment or ADAS software budgets—especially for premium and autonomous-capable vehicles. As the threat landscape matures, consumer trust and regulatory pressure will align to make V2X cybersecurity not optional but foundational. Players who can deliver scalable, compliant, and cost-effective security solutions will define the resilience and safety of tomorrow’s connected mobility networks.

Категории

Больше

"Competitive Analysis of Executive Summary Canvas Bags Market Size and Share CAGR Value The global canvas bags market size was valued at USD 1.09 billion in 2024 and is expected to reach USD 1.50 billion by 2032, at a CAGR of 4.10% during the forecast period Global Canvas Bags Market report comprises of data that can be quite essential when it comes to dominate the...

Amikor magyar nyelvű online kaszinók keresünk, általában meg vagyunk győződve róla, hogy megtaláljuk a megfelelőt a számunkra magyar online casino. A Taylor Takesa Taste kaszinóira vonatkozó tapasztalatainkban részletesen elemezzük, hogy milyen lehetőségekkel rendelkeznek az új és visszatérő...

Since its launch, Diablo 4 has managed to enthrall, challenge, and at times, frustrate its community with its dark world of Sanctuary, punishing gameplay loops, and evolving seasonal content. However, beyond its ongoing seasonal model, the future of Diablo 4 Gold remains shrouded in mystery—especially when it comes to its long-term expansion plans. With the first major expansion, Vessel...

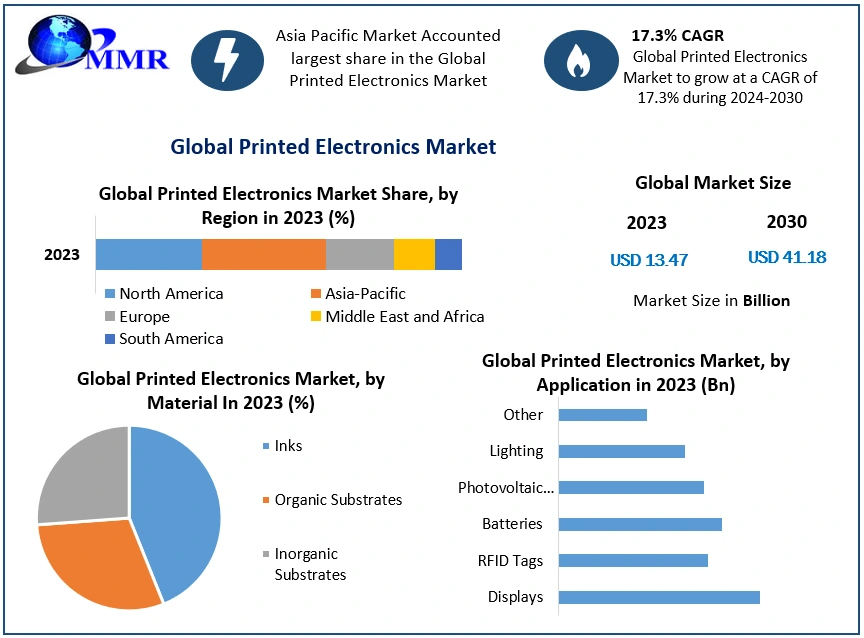

Printed Electronics Market size was valued at USD 13.47 Bn. in 2023 and the total Printed Electronics revenue is expected to grow by 17.3% from 2024 to 2030, reaching nearly USD 41.18 Bn. Printed Electronics Market Overview Maximize Market Research is a research firm. They provided an in-depth analysis of the "Printed Electronics Market". The analysis includes price considerations,...

"Executive Summary Research Antibodies Reagents Market Size and Share Analysis Report CAGR Value : Global research antibodies reagents market size was valued at USD 10.38 billion in 2024 and is projected to reach USD 16.61 billion by 2032, growing with a CAGR of 6.3% during the forecast period of 2025 to 2032. With the use of few steps or the combination of several steps,...