Antimony Market Overview: Key Applications, Technological Developments, and Competitive Landscape Analysis

The antimony market has witnessed significant growth in recent years, driven by expanding industrial applications and increasing demand across various sectors. Antimony, a critical metalloid, is primarily used in flame retardants, lead-acid batteries, alloys, and semiconductor applications. Its unique properties, including high thermal stability, corrosion resistance, and flame-retardant capability, have positioned it as an essential component in modern industries. The market is poised for sustained growth as technological advancements and industrial expansions continue to boost demand.

Market Drivers

Several factors are fueling the growth of the antimony market. One of the primary drivers is the rising demand for flame retardants in consumer electronics, construction, and automotive sectors. With stringent fire safety regulations worldwide, industries are increasingly adopting antimony-based compounds to meet compliance standards.

The expanding electric vehicle (EV) industry also contributes significantly to antimony demand. Lead-acid batteries, widely used in hybrid vehicles and stationary energy storage systems, contain antimony, which enhances battery performance and longevity. Moreover, growth in the semiconductor industry, particularly in high-performance computing devices, has created new avenues for antimony use in advanced electronics.

Emerging economies in Asia-Pacific, such as China and India, are witnessing rapid industrialization, driving construction, transportation, and electronics sectors. These developments have a direct positive impact on antimony consumption, further propelling market growth. Additionally, ongoing research in nanotechnology and energy storage applications is opening new growth opportunities for antimony-based materials.

Market Restraints

Despite promising growth, the antimony market faces certain challenges. Limited availability of high-quality antimony ores and dependence on a few major producing countries, primarily China, pose supply risks. Price volatility, driven by geopolitical tensions and fluctuating production levels, can affect market stability. Environmental and regulatory concerns associated with mining and processing antimony also restrict market expansion in some regions.

Recycling and secondary production offer partial solutions, but high costs and technological limitations hinder widespread adoption. As industries increasingly focus on sustainable practices, the antimony market must balance economic growth with environmental responsibility.

Applications and End-Use Segments

Flame retardants remain the dominant application segment, accounting for a significant share of global antimony consumption. Antimony trioxide, a key flame-retardant compound, is extensively used in plastics, textiles, and electronics to improve fire safety.

The battery industry, particularly lead-acid and emerging lithium-ion hybrid systems, represents another critical application segment. Antimony enhances grid strength and cycling performance, extending battery life and efficiency.

Other notable applications include alloys, ceramics, glass, and semiconductors. In alloys, antimony improves hardness and corrosion resistance of lead, tin, and other metals. The semiconductor industry uses antimony in infrared detectors, diodes, and thermoelectric devices, highlighting its versatility across technological domains.

Regional Insights

Asia-Pacific dominates the global antimony market due to abundant production, high consumption, and rapid industrialization. China, being the largest producer and consumer, significantly influences market dynamics. North America and Europe hold substantial market shares, driven by stringent safety regulations, automotive demand, and technological adoption. Latin America and the Middle East & Africa are emerging regions, witnessing growing industrial activity and potential opportunities for market expansion.

Competitive Landscape

The antimony market is moderately consolidated, with a few key players holding major shares. Leading companies focus on strategic partnerships, capacity expansions, technological innovations, and sustainable production practices to maintain competitiveness. Continuous investment in R&D, exploration of alternative supply sources, and development of high-purity antimony products are key strategies shaping the competitive landscape.

Future Outlook

The global antimony market is expected to maintain steady growth over the coming decade. Rising industrial demand, technological innovations, and increasing applications in electronics and energy storage are projected to fuel market expansion. However, managing supply chain risks, price volatility, and environmental concerns will remain critical for sustainable growth. Stakeholders, investors, and policymakers must closely monitor production trends, technological advancements, and regional demand patterns to capitalize on emerging opportunities.

Kategorien

Mehr lesen

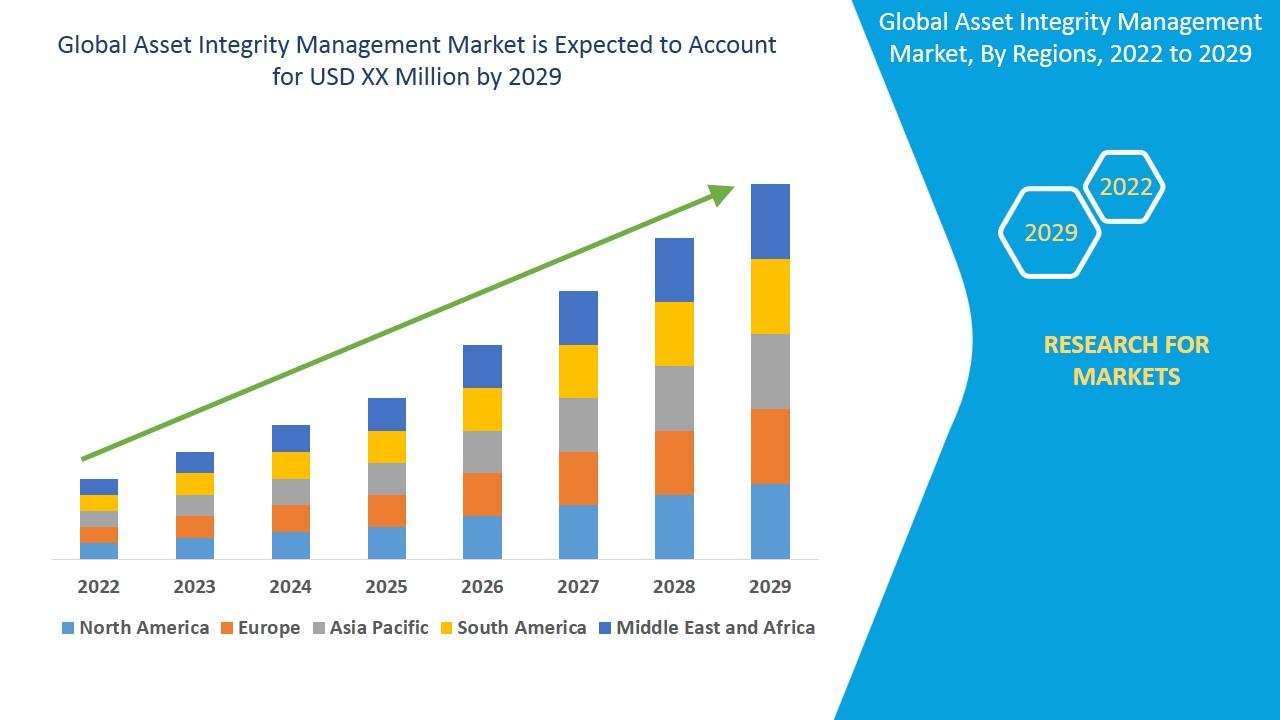

"Executive Summary Asset Integrity Management Market Size and Share Across Top Segments Asset integrity management market is expected to gain market growth in the forecast period of 2022 to 2029. Data Bridge Market Research analyses the asset integrity management market to exhibit a CAGR of 28.60% for the forecast period of 2022 to 2029. Asset Integrity Management Market report has reviews...

"Detailed Analysis of Executive Summary Keratoconjunctivitis Market Size and Share The Global Keratoconjunctivitis Market size in 2023 is 472.46 USD million. The market share is projected to grow at a CAGR of 5.31% and reach USD 730.41 million by 2031. An international Keratoconjunctivitis Market research report is planned by gathering market research data from different corners of...

PKV Games: The Perfect Blend of Tradition and Innovation in Online Gaming The online gaming world has seen tremendous growth in recent years, offering an overwhelming number of platforms and options. Yet, amidst all the new-age games, traditional card games continue to hold their charm. If you’re a fan of classic Indonesian card games and want a reliable, exciting place to play them...

"Executive Summary Middle East and Africa Magnet Wire Market : Middle East and Africa magnet wire market is expected to gain market growth in the forecast period of 2021 to 2028. Data Bridge Market Research analyses that the market is growing at a CAGR of 6.3% in the forecast period of 2021 to 2028 and expected to reach USD 2,819.99 million by 2028. Quality insights about the...

The Global CFD Trading Affiliate Programs Market size was valued at around USD2.64 billion in 2024 and is projected to reach USD7.88 billion by 2030. Along with this, the market is estimated to grow at a CAGR of around 13.11% during the forecast period, i.e., 2025-30. Global CFD Trading Affiliate Programs Market Driver: Increasing CFD Trading...