Mantengu Mining and Liberty Coal Challenge the JSE Over Alleged Share Price Manipulation

The corporate and regulatory landscape in South Africa has been stirred by dramatic accusations. Mantengu Mining has publicly accused the Johannesburg Stock Exchange (JSE) and Liberty Coal of orchestrating a scheme to depress Mantengu’s share price, alleging collusive manipulation and institutional neglect. In response, both the JSE and Liberty Coal have forcefully denied any wrongdoing and threatened legal action. The controversy has drawn the attention of regulators, law enforcement, and market participants, raising fundamental questions about market integrity, oversight, and the rights of smaller issuers. This article explores the background, the claims, the counterclaims, regulatory findings, and the broader implications of this high-stakes dispute.

Background and Context

Who is Mantengu Mining?

Mantengu Mining is a small-cap mining company listed on the JSE. It focuses on chrome and related minerals, and has publicly expressed growth ambitions, including acquisitions and expanding its production base. The company’s ability to raise capital — particularly via equity issuance — is highly sensitive to its share price. A depressed share valuation could threaten planned deals or cause excessive dilution of existing shareholders.

Liberty Coal’s Role and Connections

Liberty Coal, known for operating coal assets (notably the Optimum Colliery), became entangled when Mantengu named it among alleged co-conspirators. The controversy intensifies because Ulrich Bester, formerly Mantengu’s financial director, is now the CFO of Liberty Coal and is among Mantengu’s largest shareholders. Mantengu claims that Liberty Coal was used as a “front” in the manipulation scheme, possibly to mask ultimate beneficial ownership.

What Triggered the Dispute

Mantengu’s accusations are not spontaneous. According to its public statements:

-

It alleges a centrally controlled syndicate engaged in naked short selling of its shares (i.e., selling shares without borrowing or owning them) to artificially drive the price downward.

-

It claims the JSE refused or blocked its warnings and prevented it from publishing SENS (stock exchange) announcements, thereby suppressing detection and transparency.

-

It said the JSE borrowed shares from Mantengu’s largest shareholder, replaced them, and thereby facilitated covert trades.

-

It contends that Liberty Coal and other shell or front companies (e.g. Sable Exploration & Mining) share directors, auditors, and legal advisors to conceal the identity of manipulators.

-

Mantengu argues that depressing its share price would damage its ability to proceed with acquisitions (notably Blue Ridge Platinum) because a lower share valuation increases dilution or complicates regulatory categorisation of deals.

-

It has filed a criminal complaint with the Hawks (South Africa’s priority crime investigation unit), naming certain JSE executives, Liberty Coal, and others.

These assertions, according to Mantengu, are grounded in about 18 months of investigative work. It says it flagged the matter to the JSE earlier but was ignored or suppressed.

Responses and Regulatory Findings

JSE’s Position and Reaction

-

The JSE has denied any complicity, insisting it acts in accordance with the Financial Markets Act and its statutory duties.

-

It issued a cease and desist letter demanding retraction of defamatory statements and apology, warning that continued allegations would prompt legal action.

-

The JSE says it cannot publicly disclose internal surveillance or investigation details due to confidentiality obligations.

-

It insists that securities lending and borrowing are legitimate market tools and do not necessarily indicate manipulation.

-

It claims that it either found no evidence of manipulation worth referral to the FSCA, or the matter is under FSCA investigation.

-

It rejects the charge that it suppressed Mantengu’s SENS announcements, arguing that the responsibility for such announcements lies with the company and its sponsor, subject to listings requirements.

Liberty Coal and Bester’s Response

-

Liberty Coal dismisses the allegations as baseless and defamatory. It demands an apology and threatens litigation seeking damages (in fact, it has initiated a R250 million claim for defamation).

-

It describes the claims as “delusional fantasies” and accuses Mantengu’s CEO of speculation without substantiation.

-

Ulrich Bester denies manipulating the share price, noting that depressing the value would hurt his own holdings.

FSCA Investigation and Findings

-

After a months-long probe, the Financial Sector Conduct Authority (FSCA) concluded it found no evidence of naked shorting in Mantengu’s stock and no improper conduct by the JSE or its officials.

-

The FSCA stated that the transactions Mantengu flagged were consistent with lawful securities trades.

-

However, Mantengu has objected to the scope of the FSCA’s review, noting that it covered only nine months (out of a 24-month period) and excluded certain data (e.g. electronic devices seized under court orders), which the company says weakens the findings.

-

Mantengu also argues the FSCA focused narrowly on short selling rather than broader collusive manipulation across multiple entities.

Thus, while the FSCA cleared important ground, the parties remain in conflict, and larger legal and law enforcement proceedings may yet weigh on the dispute.

Key Issues & Challenges

Market Integrity and Confidence

If Mantengu’s allegations are upheld, the case would expose serious vulnerabilities in exchange surveillance, regulatory enforcement, and institutional accountability. This could undermine investor confidence, especially in smaller, less scrutinized issuers.

Power Imbalance Between Small Issuers and Exchanges

Small or mid-cap companies often depend on fairness of markets yet lack the influence or resources to demand transparency from exchanges. This dispute highlights those asymmetries.

Defamation Risk vs. Duty to Inform

By naming individuals and entities publicly, Mantengu carries risk of defamation liability if its allegations cannot be sustained in court. Balancing investor warning obligations and legal exposure compounds the challenge.

Regulatory and Enforcement Gaps

The FSCA’s finding, whether accepted or not, raises questions about whether its investigative scope and authority are sufficient to detect complex conspiracies. Whether law enforcement (Hawks) will move and how thoroughly is uncertain.

Implications for Capital Raising and Strategy

Mantengu’s capacity to execute acquisitions or raise equity depends heavily on its stock valuation. Prolonged uncertainty or damage to its reputation could impede its growth trajectory.

Frequently Asked Questions (FAQs)

What is “naked short selling,” and why is it controversial?

Naked short selling involves selling shares without actually owning or having borrowed them to deliver on settlement. Because such practice can artificially drive down prices, it is prohibited or heavily regulated in many jurisdictions. Mantengu alleges that naked short selling was used against it to suppress its share price.

Does the FSCA’s conclusion mean Mantengu’s claims are false?

Not necessarily. The FSCA’s investigation cleared Mantengu’s flagged trades as lawful in the period it reviewed, but Mantengu disputes the scope and exclusions of the inquiry. The matter is not entirely settled, especially because law enforcement processes may uncover further evidence.

Can Mantengu force the JSE to publish disclosures it claims were blocked?

Yes — Mantengu has initiated court action (in the Gauteng High Court) seeking an order compelling the JSE to publish a SENS announcement it says the JSE refused to accept. Whether the court grants that relief depends on legal interpretation of the stock exchange rules and obligations.

What are the legal risks for Mantengu in making public accusations?

If Mantengu cannot substantiate its claims, it could face defamation lawsuits, damages claims, and negative reputational consequences. Indeed, Liberty Coal has already demanded R250 million in damages for defamation. Mantengu must tread carefully between disclosure and liability.

What lessons does this dispute offer for capital markets in emerging economies?

It underscores the importance of strong, independent exchange governance, robust surveillance systems, clear rules around short selling, and the need for regulatory bodies with teeth. It also highlights the vulnerability of smaller issuers to possible institutional unfairness or opacity.

Conclusion

The clash between Mantengu Mining, Liberty Coal, and the JSE over alleged share price manipulation is more than a personal vendetta — it is a test of South Africa’s capital market architecture. For Mantengu, the stakes are existential, as it seeks to defend its valuation, acquisition strategy, and reputation. For the JSE and Liberty Coal, defending legitimacy and denying collusion are equally critical.

While the FSCA has publicly cleared key actors, the dispute is not over. Mantengu contests the narrow scope of regulatory inquiry and insists on further scrutiny. Legal proceedings and law enforcement investigations may yet unearth deeper evidence or settle contentious questions.

Whatever the outcome, this dispute will leave a lasting imprint: it may prompt stronger disclosure and surveillance rules, sharpen the balance between issuer rights and exchange authority, and reinforce the need for regulators to act transparently and decisively. In public markets, perception and trust matter as much as facts. The ultimate resolution of this case will speak volumes about how South Africa — and emerging capital markets more broadly — protects fairness, holds institutions to account, and maintains confidence in the system.

Kategorien

Mehr lesen

Laser Welding Machine Market Demand: Overview, Scope, Dynamics, Drivers, Restraints, Segmentation, and Regional Analysis Overview of the Laser Welding Machine Market The laser welding machine market Demand is a rapidly growing sector in industrial manufacturing, driven by the increasing demand for precision, efficiency, and automation in welding processes across various industries. Laser...

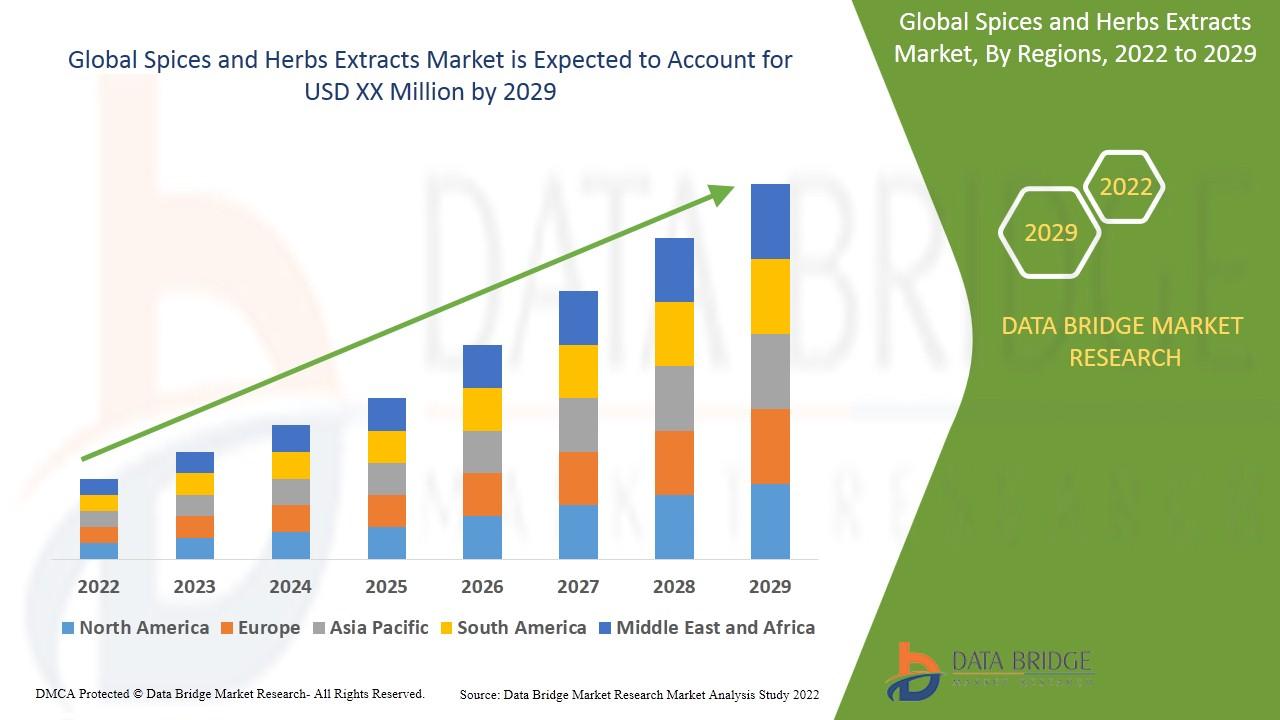

Comprehensive Outlook on Executive Summary Spices and Herbs Extracts Market Size and Share The spices and herbs extracts market is expected to witness market growth at a rate of 7.6% in the forecast period of 2022 to 2029. This competitive era calls for businesses to be equipped with knowhow of the major happenings of the market and Spices and Herbs Extracts Market This Spices and Herbs...

"Executive Summary Cast films Market : Global cast films market size was valued at USD 8.57 billion in 2024 and is projected to reach USD 11.25 billion by 2032, with a CAGR of 3.46% during the forecast period of 2025 to 2032. The Cast films Market report contains market insights and analysis for industry which are backed up by SWOT analysis. This market research...

In a world where first impressions matter, the way your email looks says a lot about you. Whether you’re a business owner, freelancer, or job seeker, having your Own Custom Email Address can make a powerful impact. Think about it—would you trust an email from johndoe@gmail.com or john@doedesign.com more? The second one instantly feels more professional and trustworthy. That’s...

Sharjah is one of the UAE’s most vibrant emirates, offering a perfect balance between tradition and modern living. Known for its cultural landmarks, bustling souks, family-friendly attractions, and close proximity to Dubai, it has become a favorite destination for residents and tourists alike. Whether you’re here for work, leisure, or long-term living, one of the best ways to...